Opportunities With Mid-Tier And Junior Royalty Companies – Part 7

Excelsior Prosperity w/ Shad Marquitz – 07-14-2024

Welcome back to another update reviewing the opportunities in the mid-tier and junior royalty companies. In the first 6 articles in this series, we established the key value drivers, diversification advantages, risk mitigation advantages, and opportunities for accretive growth over time in the royalty and streaming companies.

Thus far we have highlighted 7 companies in this category:

Sandstorm Gold (SSL.TO) (SAND), Metalla Royalty & Streaming (TSX.V:MTA – NYSE:MTA), Elemental Altus Royalties (TSXV: ELE) (OTCQX: ELEMF), Vox Royalty Corp (TSX:VOXR) (NASDAQ:VOXR), Trident Royalties (AIM:TRR – OTC:TDTRF), Triple Flag Precious Metals (TSX: TFPM) (NYSE: TFPM), and EMX Royalty Corp (TSX.V: EMX) (NSYE: EMX).

Here is a link to [Part 1]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior

Here is a link to [Part 2]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-6b8

Here is a link to [Part 3]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-f34

Here is a link to [Part 4]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-1e5

Here is a link to [Part 5]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-9f8

Here is a link to [Part 6]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-92a

Here in [Part 7] of this series, we’re going to review a number of different exclusive interviews and news updates on some of those companies, as well as introduce an 8th diversified royalty company.

So let’s get into it…

The first company we ever discussed in this series was Sandstorm Gold (SSL.TO) (SAND), and last month I had a great high-level conversation with David Awram, Sr. Executive Vice President, Co-Founder, and Director of Sandstorm Gold.

Sandstorm Gold – Review Of Q1 Financials And Operations And Key Royalty Partner Project Updates – June 11, 2024

David and I reviewed the key takeaways from Q1 2024 financials and operations. We also got into many of the key royalty partner projects feeding into the larger growth profile over the next 5 years for this mid-tier precious metals royalty company. Sandstorm Gold is diversified across 250 royalties, 40 producing assets, exploration optionality, different jurisdictions, and has a leading cost profile from producing royalty partners.

This is wide-ranging discussion that gets into the value proposition and differentiating attributes of Sandstorm Gold within it’s peer group of royalty companies. We spend some time unpacking some of the key projects they hold royalties on that are partnered with senior mining companies as operators, that are well capitalized to have more exploration and development upside than the market is anticipating. Some of the projects Dave outlined were the Houndé Project operated by Endeavour Mining, the Bonikro Project operated by Allied Gold, the Barry Project operated by Bonterra Resources (that is being combined with Osisko Mining’s Windfall Project), and Caserones operated by Lundin Mining.

Next we got into some of the large development projects that are moving down the development pipeline and into production, as big contributors to future gold equivalent ounces and revenues. We reviewed how Equinox’s Greenstone Mine has just had first gold pour, as the 4th largest gold mine in Canada and a big win for Sandstorm and the Canadian mining sector at large. Next Dave highlighted a recent site visit to Ivanhoe Mining’s Platreef Project in South Africa, and how construction is well underway to bring this mine into commercial production by next year. We then reviewed the cornerstone Hod Maden royalty asset in Turkey, and how the terms on this asset and conversion into a gold stream have changed over time, including the sale of the 30% interest in the project to Horizon Copper Corp. Lastly we wrap up with a look ahead to the Mara gold stream operated by Glencore, as an example of how a royalty purchase can change hands and become incredibly value-accretive.

Metalla Royalty & Streaming – Q1 Financial Recap, Near Term Growth Outlook – June 19, 2024

Brett Heath President and CEO of Metalla Royalty & Streaming (TSX.V:MTA & NYSE:MTA), joined us last month over at the KE Report to recap the Q1 financial results and outline key growth assets into 2025. Brett outlined the company’s reported Q1 2024 earnings of $1.3 million from five producing assets.

The conversation then shifts to Metalla’s growth prospects, highlighting a number of assets that will be moving into production through the end of 2025 and generating cash flow for the Company. We also discuss the acquisition and capital allocation strategy to acquire new royalties that would move the needle for the Company. Brett underscores the Company’s long-term strategy of focusing on high-quality, long-life assets.

Elemental Altus – Q1 2024 Financials, A Royalty Acquisition, And Royalty Partner Updates – June 6, 2024

Fred Bell, CEO of Elemental Altus Royalties (TSX.V:ELE – OTCQX:ELEMF), joins me to review their operational and financial results from Q1 2024, a recent royalty acquisition now partnered with Rio Tinto, and a few royalty partner updates. We start off diving into the key metrics and takeaways from the first quarter financials.

2024 Outlook

Diba remains on track to be the Company’s newest producing gold royalty. Allied Gold Corp (TSX: AAUC) have announced that mining is expected to commence in Q2 2024

Elemental Altus on course to meet guidance of 10,000 to 11,700 GEOs as production increases over the year. This guidance represents at its midpoint a 19% increase on 2023 and provides top-line exposure to gold and copper prices

Repaid US$5 million debt in Q1 2024, leaving US$25 million undrawn on the credit facility and with approximately US$9 million cash on quarter end prior to Q1 royalty receipts. The Company intends to continue to reduce the amount drawn on the credit facility while maintaining financial flexibility to make new acquisitions

Falling G&A expenditure and significant expected cash flow generation following merger synergies and asset sales, which are also expected to generate milestone payments placing the company in a position to generate material cash flow.

During the interview we reviewed their increasing revenue and expanding margins over the course of 2024, and why the company strategy was to aggressively go after cash-flowing assets. We then highlighted that the Diba royalty is on track to commence mining in Q2 and has the potential to be a material long-life royalty for the company based on the exploration potential once it is in production. Fred discusses how this complements other long-life royalty assets like Karlawinda and Caserones, as key cornerstone assets.

We also discussed the large portfolio of development and explorations assets that will provide discovery optionality to future value creation. To that point we discussed the recent acquisition of a royalty over a Rio Tinto operated lithium project in Rwanda, where the Company expect to see significant news flow over the course of 2024. The company is cashed up and looking to make more accretive acquisitions over the course of this year.

Vox Provides Project Updates for Plutonic East, Bulong and Koolyanobbing, Including Timing Estimates for First Gold Production - July 2, 2024

https://www.voxroyalty.com/_resources/news/2024/nr-20240702.pdf

• Black Cat announced that key site development activities have commenced at the Myhree Gold Project, following the recent announcement of turn-key contractor mining and third party tolling agreements, which is expected to result in royalty-linked ore being processed at the Paddington processing facility from September 2024 onwards;

• Catalyst announced that dewatering activities at the Plutonic East underground gold mine workings were underway and progressing ahead of schedule, ahead of anticipated first production in Q1 2025;

• MinRes announced a decision to ramp down and cease operations at their Yilgarn Hub (including Koolyanobbing) by December 31, 2024, following the conclusion of a comprehensive evaluation.

• Bulong (Construction – Western Australia) – Commencement of Mining Development Activities at Myhree, First Production Expected in September 2024. Vox holds an uncapped 1.0% net smelter royalty over key areas of the Bulong Mining Centre, part of the Kal East Gold Project, including the Myhree and Boundary deposits.

EMX Royalty Corp – Multiplicative Optionality Across 170 Precious Metals And Critical Minerals Royalties – 06-27-2024

Dave Cole, President and CEO of EMX Royalty Corp (TSX.V: EMX) (NSYE: EMX), joins me for a comprehensive update on their distinguishing value proposition in the royalty space, a number of copper, gold, and critical minerals partner project updates, a number revenue-generating pre-production royalties, a review of Q1 financials, and the balance between further paying down debt in tandem with buying back Company shares.

We start off discussing the multi-prong approach of generating revenues from existing properties optioned off to other operators, and then creating royalties, in addition to buying royalties in the market when the right value accretive dynamics are in place. At present EMX Royalty has 6 producing royalties and around 50 other royalties bringing in revenues from defined pre-production payments, option payments, and gate payments.

Next we discussed the substantial copper exposure and incoming cashflows that EMX has coming in from both the Caserones Project in Chile operated by Lundin Mining, and the Timok Project in Serbia operated by Zijin Mining, and as cornerstone generational assets. With regards to the producing gold royalties, Dave first outlines how the Gediktepe Mine in Turkey is throwing off great revenues from gold, but then will be transitioning to a polymetallic deposit in the years to come. Then he also outlines the stable gold production and long-life asset in the Leeville Mine in Nevada, operated by Nevada Gold Mines (the JV between Barrick Gold and Newmont Mining).

This leads into a broader discussion about how important it is to have quality operating partners on the royalty projects; leading us into a few more partner updates with South32’s $2.16Billion at the polymetallic Peake deposit on the Hermosa Taylor Project in Arizona, and the development-stage copper-iron-gold Viscaria project in Sweden, operated by Copperstone Resources.

We then shift over to reviewing the 44 other pre-production royalties that are still generating revenues via lease-option payments, stage-gate payments to advance properties, advanced minimum royalty payments, and that come in by way of cash and often times shares in partner companies. We do a brief review of Q1 financials and strength of the company, as well as have Dave break down the balance between paying down debt with buying back company shares, since the company is still trading below it’s net asset value.

Wrapping up we discuss the synergistic relationship between EMX Royalty and Franco-Nevada (FNV) where not only are they the new lender of choice for their recently announced $35 Million Loan, that clears out the prior Sprott loan, but Franco-Nevada has an investment stake in EMX, has syndicated royalty purchase agreements together in the past, and there is an ongoing joint venture partnership to acquire earlier-stage gold and copper royalties sourced by EMX.

Now let’s introduce the 8th company in this series, Ecora Resources (TSX: ECOR) (LSE:ECOR) (OTCQX:ECRAF).

I’ve been following this company since back when they were called AngloPacific, and have really been impressed with the transition they’ve made into a growing diversified royalty company, more akin to Altius Minerals or EMX Royalty with a mix of different metals and commodities. In the past, when shifting over from Anglo Pacific to Ecora Resources, this company received lower valuation metrics due to this legacy metallurgical coal. However, over time the cashflow complexion has been changing and will continue transitioning over to more of a 100% focus to future facing commodities critical for the energy transition and critical minerals.

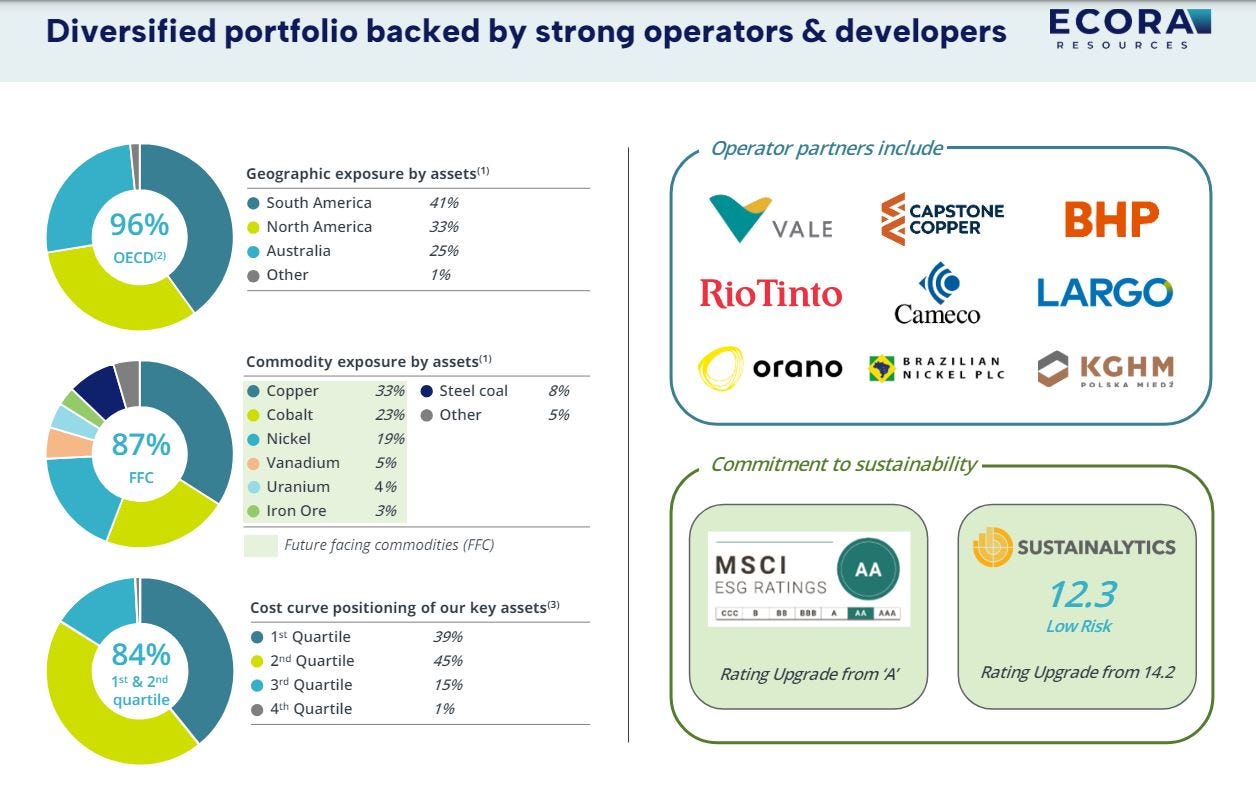

We’ve talked about one of the advantages of investing in royalty companies over individual miners is their diversification in assets, jurisdictions, and operators. Ecora’s commodity exposure through their royalty portfolio now has over 33% exposure to copper, 23% to cobalt, 19% to nickel, 8% to met coal, 5% to vanadium, 4% to uranium, 3% to iron ore, and 5% to other commodities like rare earths (as noted by their new acquisition announced this month). These royalties are mostly spread out through South America, North America, and Australia, and with senior mining companies that have 1st and 2nd quartile low costs for their operations.

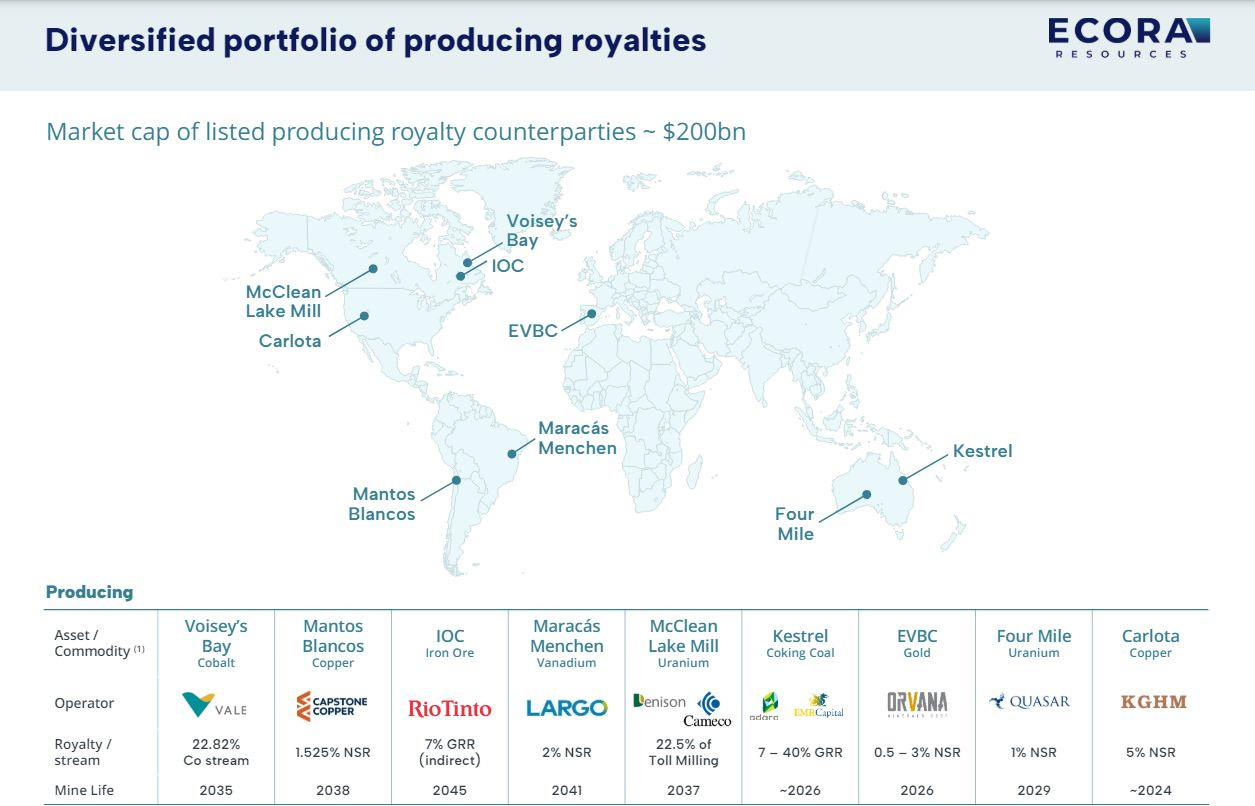

At present the company has 9 producing assets that are driving in the revenues:

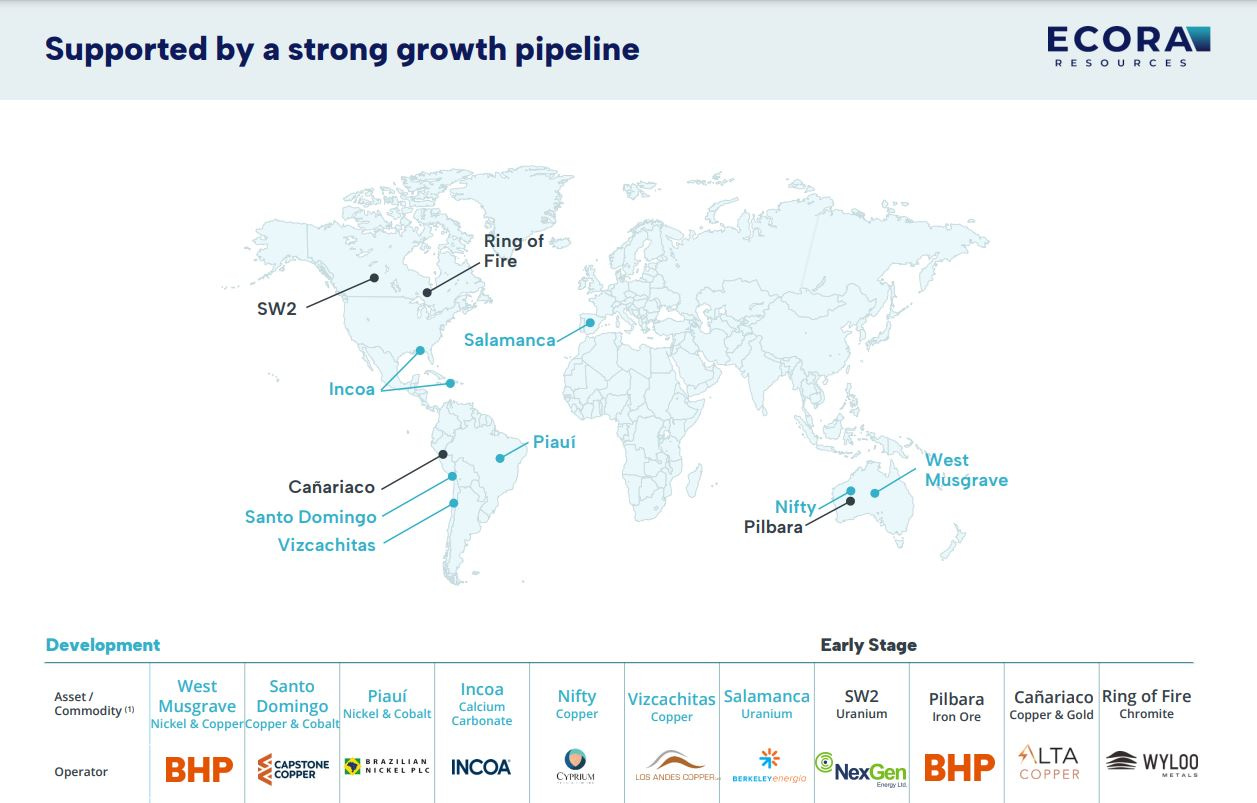

One project that had not made it onto those maps yet, as a development stage project, because it was a new acquisition just made this month is the Phalaborwa Rare Earths Project, operated by Rainbow Rare Earths Ltd (LSE: RBW) in South Africa. This is their 22nd royalty and the press release is included below for quick reference.

Acquisition Of Royalty Over The Phalaborwa Rare Earths Project – July 1, 2024

https://www.ecora-resources.com/application/files/8717/1977/9300/Rainbow_FINAL.pdf

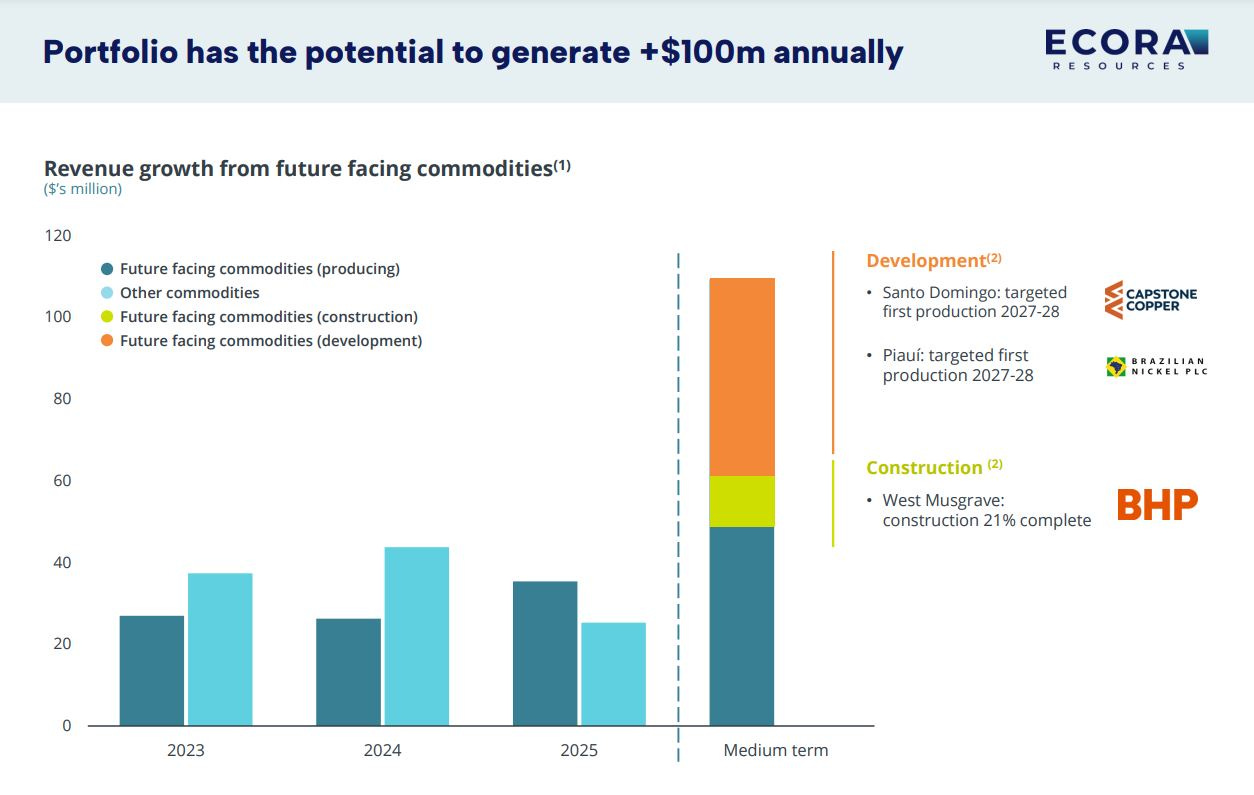

It is compelling to see how the West Musgrave Project, operated by BHP, and 2 of the key development projects, Santo Doming, operated by Capstone Copper, and Piaui’, operated by Brazilian Nickel Plc, will be contributing to future revenue growth by 2027-2028.

Marc Bishop Lafleche, CEO and Executive Director of Ecora Resources, joined me earlier this month, over at the KE Report, to provide a comprehensive overview of their 22 royalty and streaming assets, across 5 continents, providing diversified future-facing commodities exposure to the metals critical for the energy transition.

Ecora Resources – Comprehensive Update On Their Portfolio Of 22 Royalties Focused On Future-Facing Commodities – July 1, 2024

Marc outlines some of the key contributing projects and operating partners like Vale, BHP, Capstone Copper, Rio Tinto, Brazilian Nickel, Largo, Cameco, Orano, NexGen, and Rainbow Rare Earths, as it relates to their critical minerals exposure. We highlight a few of the key royalties of the 9 producing assets, and 13 other development-stage and exploration-stage assets, the strength of their operating partners, the low-cost and long mine-life projections, that also have low carbon intensities.

Wrapping up we look into the financial strength of the incoming revenues, with the transition from the traditional to the more energy metals focus over the next few years in producing and near-production asset, and the credit facility to be able to execute on future accretive acquisitions. Additionally, Marc outlines the key stakeholders in Ecora Resources, and their capital allocation strategy balanced between deleveraging debt, paying a dividend, and buying back shares.

That’s it for this [Part 7] in this evolving series on junior and mid-tier royalty and streaming companies, and there will be a number more of these articles on this topic in the weeks and months ahead.

As always, thanks for reading and may you have prosperity in your trading and in life!

- Shad