Opportunities With Mid-Tier And Junior Royalty Companies – Part 6

Excelsior Prosperity w/ Shad Marquitz 06/29/2024

Welcome back to another update reviewing the opportunities in the mid-tier and junior royalty companies. In the first 5 articles in this series, we established the key value drivers, diversification advantages, risk mitigation advantages, and the large net asset value per employee found in the royalty and streaming companies.

We also have previously highlighted the first 4 primary companies in this category, that I also hold in my portfolio (so I’m biased in that sense) by taking deeper dives into their value propositions:

Sandstorm Gold (SSL.TO) (SAND), Metalla Royalty & Streaming (TSX.V:MTA) (NYSE:MTA), Elemental Altus Royalties Corp. (TSXV: ELE) (OTCQX: ELEMF), and Vox Royalty Corp. (TSX: VOXR) (NASDAQ: VOXR).

[Part 5] was really a mashup of news updates from the first 4 companies, a teaser for the 5th company (which will be featured in this article), and then I included 2 other exclusive interviews we did over at the KE Report with Trident Royalties (AIM:TRR – OTC:TDTRF) and Triple Flag Precious Metals (TSX: TFPM) (NYSE: TFPM). We didn’t take deep dives into those 2 companies, but did get a basic overview of each, and included a slide for each highlighting a map of their key global royalty assets. The interviews themselves provided readers here with the chance to hear those value propositions directly from the mouths of the CEOs of their respective companies. Hopefully folks invested the 15-20 minutes of time to digest both Triple Flag PMs and Trident Royalties interviews. So now we’ve touched upon 6 mid-tier and junior royalty stocks in total during this series.

Opportunities With Mid-Tier And Junior Royalty Companies – Part 5

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-9f8

I don’t have positions personally in those 2 companies featured in the last article, but was invested in Triple Flag in the past, after they took over Maverix Metals in early 2023. Having said that, I’ve considered dropping some future profits from other winning resource trades into both of them, for safer gradual value accretion over time. Both Triple Flag and Trident have compelling portfolios for consideration; however, it is possible that Trident is in the process of being acquired by Deterra Global Holdings Pty Ltd. based on a press release from June 13th.

https://polaris.brighterir.com/public/trident/news/rns/story/rmdp89r

We’ll have to keep following along with that potential takeover news to see how things develop. To that point, from time to time, I’m going to continue including interviews and brief write-ups with other royalty companies that are not held in my portfolio, because there really are some solid companies with attractive asset portfolios in this sector.

It’s good to always be building a watchlist of quality companies.

My perspective in talking to resource investors for the last 15 years is that most people are critically underexposed to the royalty and streaming resource companies, and are taking on far too much risk putting all their eggs into only the speculative junior mining stocks.

To this very point: Earlier this week, in a conversation with a fellow investor I respect a great deal, we were discussing that royalty companies are one of the smartest allocations of capital in the resource space. However, their reflection was that there just isn’t enough torque in them to feed their particular speculative urges. I laughed and understood what they meant. Now, to be clear, there are some big swings in the stock prices of royalty companies, from time to time, that can be exploited. Overall, individual mining companies really are much more volatile though… especially the juniors. However, my response back was that royalty companies really fit a different niche in one’s resource portfolio, for more of a longer-term “slow and steady wins the race” value investment. They hadn’t considered that, because to them everything was a swing-for-the fences trade. Both strategies are worth having exposure to.

Personally, I’m not buying into these royalty companies noted in this particular series for penny-flipping or swing-trading just to play a particular news catalyst. Now, for clarity, I do position-trade in royalty companies over intermediate-term technical moves, when I feel they get too oversold and load up, and then may trim some back off the top when they get more richly valued. However, these are generally core anchor positions in my portfolio, with the strategy of holding them for long periods of time (many years… not just days or weeks or months).

My speculative urges (the gambler in me) are fulfilled buying smaller allocations into exploration drillplays, or development-stage optionality plays that may suddenly get rerated higher, or even smaller growth-oriented producers that may surge with metals prices as their margins and resources expand. I then peel off a portion of the profits from those winning trades in individual mining stocks, and then store them in royalty companies; like people used to store up food preserves in mason jars, or like people store longer-term wealth into gold and silver.

That is the benefit of royalty companies… you don’t have to get hung up on if the company is going to sink or sail on every single news release. Having said that, there are occasionally critical news releases for any given royalty company that can cause them to be rerated higher or lower for the near-term. Over the fullness of time, their basket of assets and operating partners are continuing to develop and de-risk projects, ultimately moving more assets towards production. Additionally, some of their solid producing assets are also still expanding and operators are finding more reserves or increasing production output. People need to think about royalty companies in terms of value accretion over years or even decades, not as “what have you done for me lately” speculative trades.

As this commodity cycle matures, and when the gold, silver, copper, nickel, pgms, uranium, oil, and nat gas companies have hit their major highs respectively, my personal long-range plan is to eventually pull in my horns from speculating on mining stocks, and just dump those profits into a portfolio of solid dividend-paying larger commodity producers and the diversified royalty and streaming companies. There have been a number of people that have asked me what my “end-game” is? That’s my end-game.

In this article we are going to take a look at the next royalty company in this category, EMX Royalty Corp (TSX.V: EMX) (NSYE: EMX).

I have been following this company’s success for a long time (over a decade), but had never moved it from my watchlist over into my portfolio until early November 2022. That November, I was attending our friend and colleague, Brien Lundin’s, New Orleans Investment Conference (which is a highly recommended event). While at the conference I had a number of good conversations with CEO, David Cole, and the now retired Director of Investor Relations, Scott Close, at their company booth; and later at a mixer in the hotel lounge.

They hosted an investor dinner the following evening during the conference, where I attended and asked a lot of questions about their portfolio, how they balance the prospect generator model cost and timelines with the option of just buying existing royalties, and how they internally valued royalty assets. Dave’s answers included an internal study they had conducted on the value of “discovery optionality,” and the true longer-term value of the royalties really made an imprint in my mind about the royalty sector’s larger potential. Dave is one of the sharpest individuals in the junior resource sector, and if anyone takes the time to engage him, he will not disappoint.

Dave and Scott and another savvy fund manager were all patient and instructive with my myriad of questions, as we enjoyed a fantastic dinner and conversation together. I fired off all kinds of scenarios about assets held in other royalty companies, and also within their own EMX royalty portfolio. Dave was incredibly candid and congratulatory about the fantastic deals that had been executed in a number of their peer royalty companies within the sector. He was also critical of some individual deals when warranted, and explained his thought process about when companies may have overpaid or miscalculated future returns. He was also very transparent about their good and bad decisions as a company over time, what they’ve learned moving forward, and what the future growth will look like as the next few years unfolded.

I left that conference impressed, and got positioned in EMX Royalty upon returning home in November of 2022, and have added to the position a few more times, (most recently in early February of this year at $1.48), with an average overall cost-basis of $1.73 per share. EMX closed on Friday at $1.80, so I’m up a whopping 4% overall in the position after a year and half of building a position. I realize that is not a great success story so far and I’ve not gotten rich enough to sail off into the sunset on this investment (yet…). The reason for sharing this information with you is to highlight that clearly I believe this current pricing level is an attractive valuation for accumulation, and my expectations are for a MUCH higher shareprice level in the years to come. {This is not investment advice… I’m not recommending anyone else buy this stock here… and I’ve not been commissioned by this company to write this piece… I’m just sharing with readers my thoughts, approach, and personal thesis.}

So, let get into it…

The company currently has 6 producing assets:

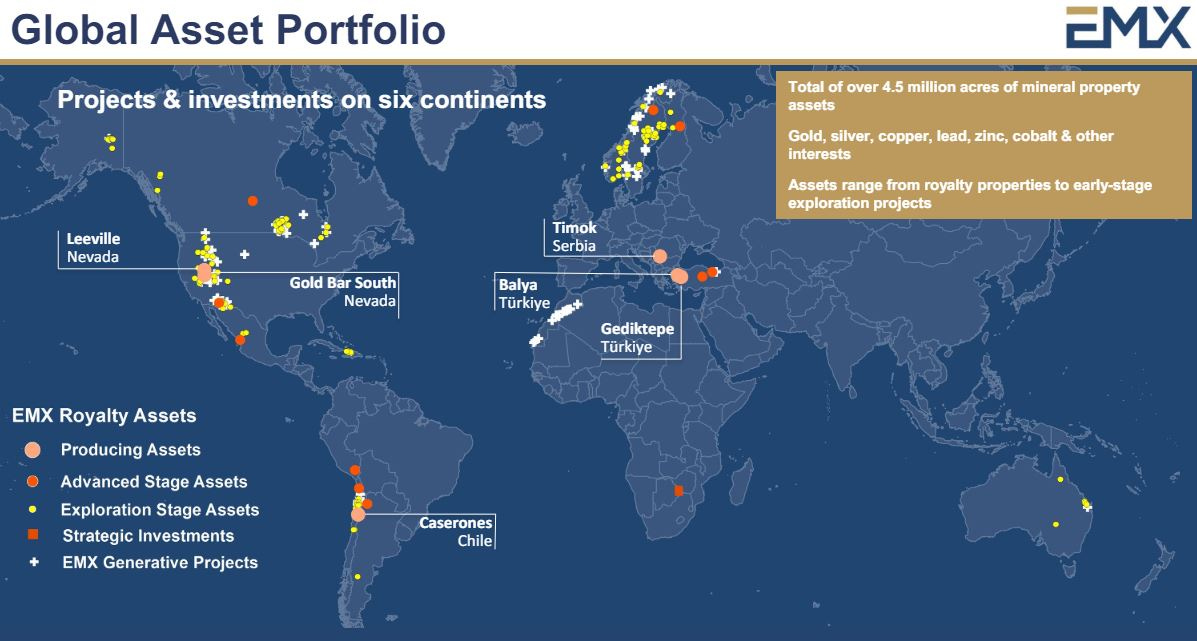

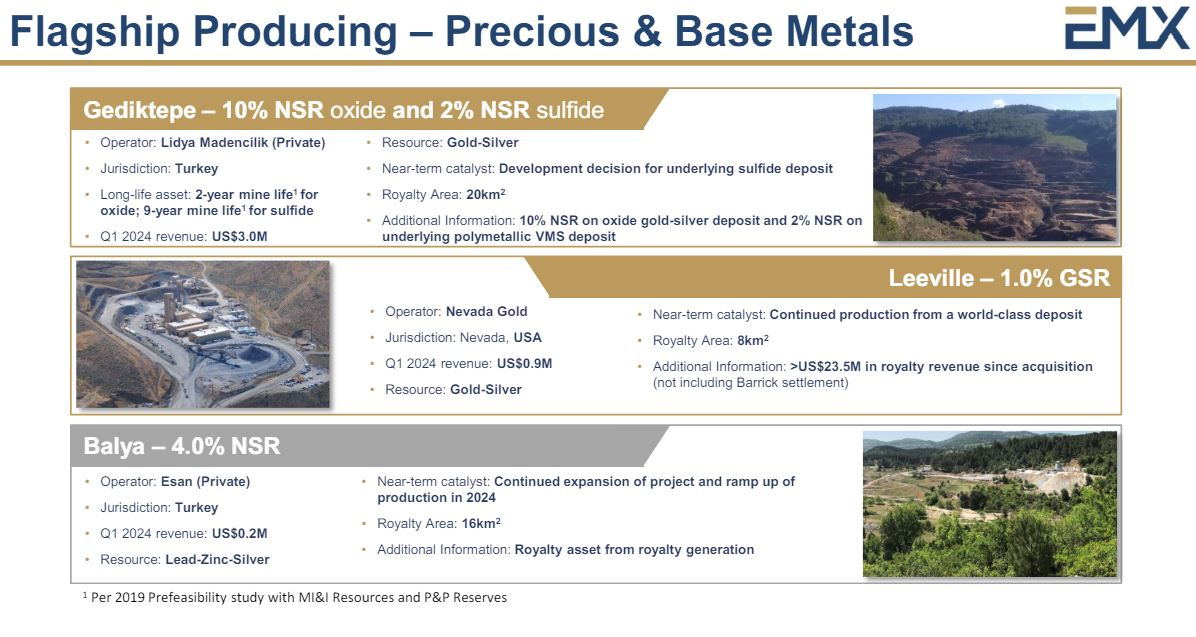

Timok in Serbia, Balya and Gediktepe in Turkey, Caserones in Chile, along with Leeville and Gold Bar in Nevada. We’re going to dig into those later in this article.

Here is a comprehensive list of the 170+ royalties that the company holds in their portfolio. This table list provides the project, operator, location, type of commodity, and amount of the royalty and/or payments on each asset:

Here is a fun interactive map of their company assets that can be zoomed in on, and if you hover over each one get more information about that project, operator, and royalty or if it is available for option.

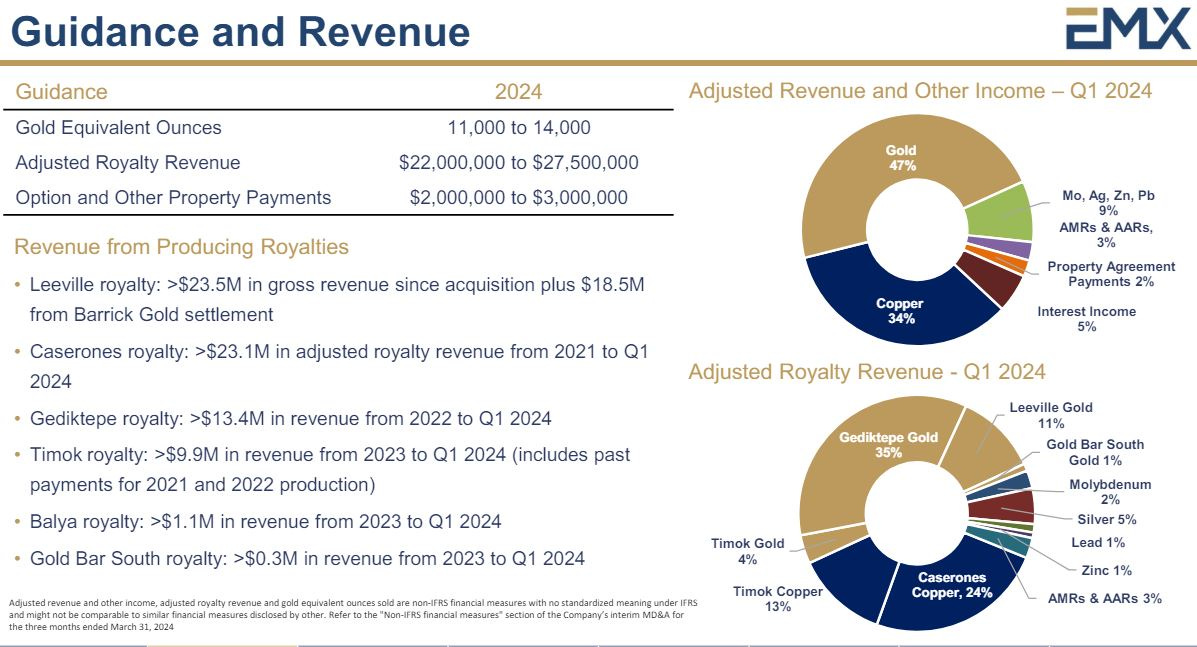

One can see in the slide above that the 2024 guidance is for 11,000 – 14,000 gold equivalent ounces to be produced, with $22M-$27M in adjusted royalty revenue, and another $2M-$3M from royalty option payments or other stage-gate payments. The larger contributors to date have the Leeville royalty, Caserones royalty, Gediktepe royalty, and the Timok royalty, and they will remain strong contributors (with a brief transition coming up from Gediktepe next year from more gold focused to more base metal focused). We can also see that EMX Royalty is diversified across mostly copper and gold, but with additional contributions from silver, molybdenum, lead, and zinc.

Interestingly, I rarely if ever hear about EMX or other royalty companies with nice exposure to the red metal as being great ways to play the longer-term copper bull market… but they absolutely are…

While EMX has plenty of copper exposure, they are also very well exposed to gold.

Another point of consideration for EMX is that, aside from their 6 producing project royalties, they also have ~44 other pre-production royalties that are also generating incoming revenues for the company. The company is generating these revenues via lease-option payments, stage-gate payments to advance properties, advanced minimum royalty payments, and these come in by way of cash and/or shares in partner companies. That’s where that “Option and other payments” revenue is coming from.

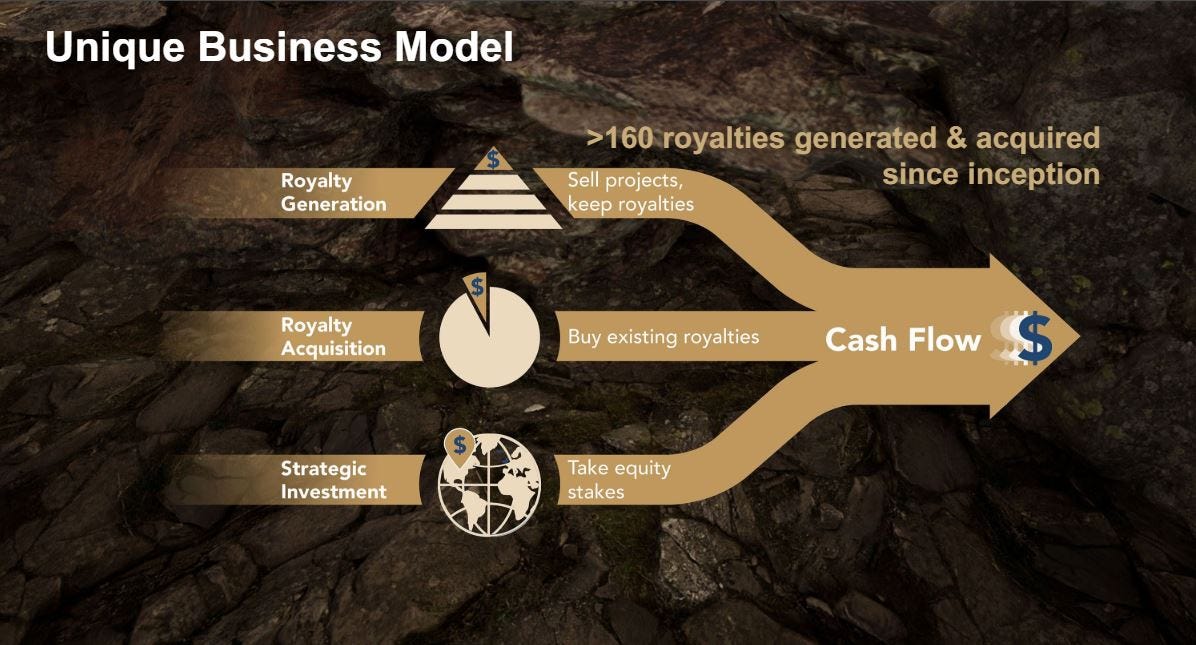

This slide above is a little dated (in that it only shows 160 royalties instead of 170+), but clearly outlines the triple-pronged approach of value creation:

1) Generating royalties, option payments, stage-gate payments, and other payments by way of their prospect generator model. They do the early-stage identification and exploration and then bring in option partners or sell the projects; but always retaining a royalty.

2) They directly acquire 3rd Party royalties that are producing or moving down the exploration and development pipeline towards production.

3) They make or take strategic investments in partner company operators as a means of experiencing the upside of those companies value creation, that can then be cashed in on a later date.

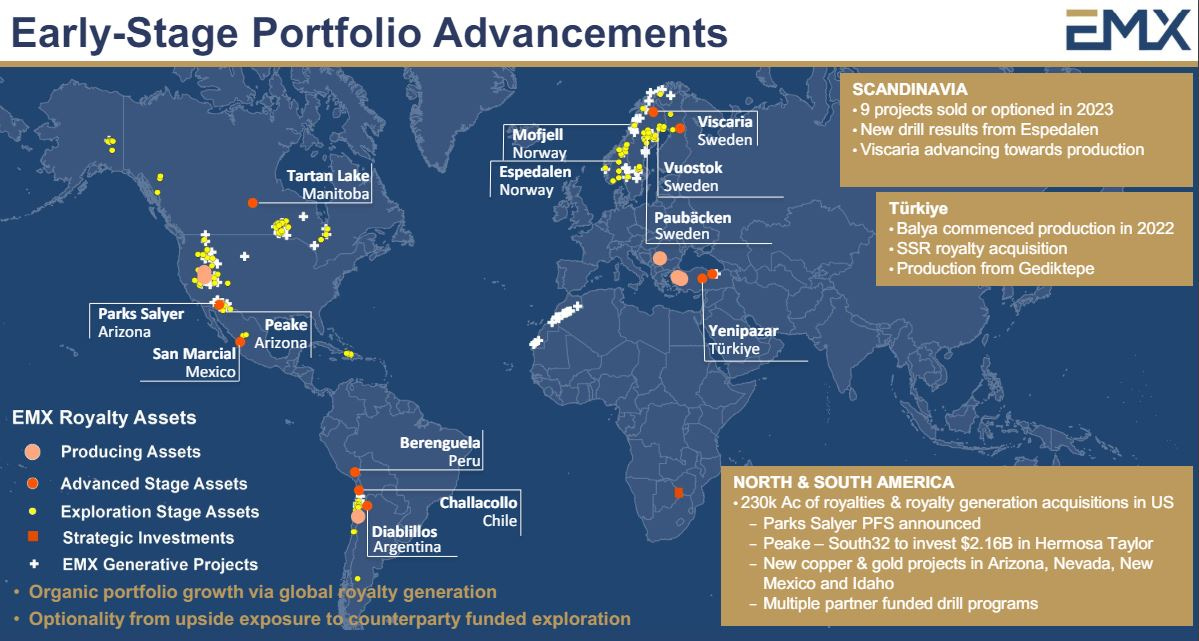

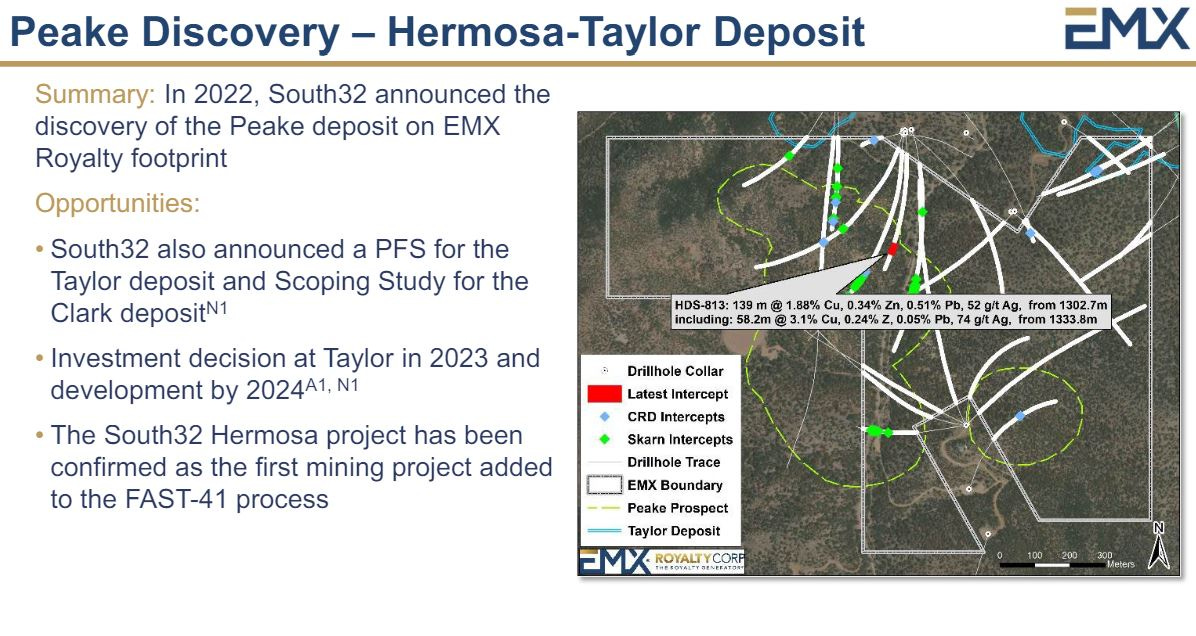

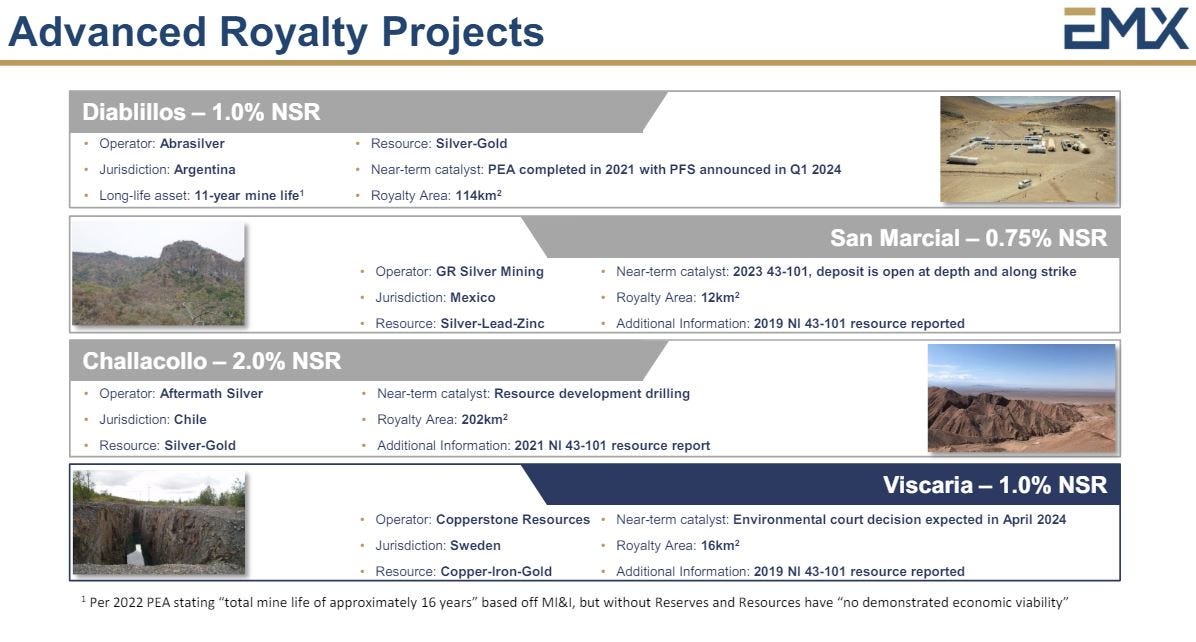

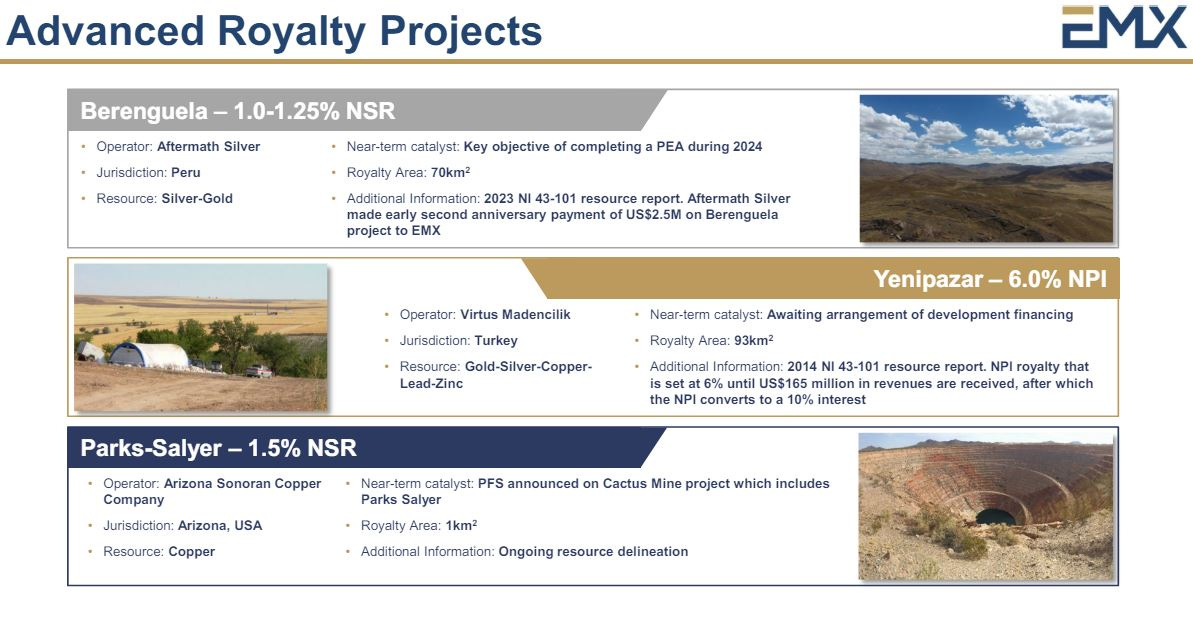

Next, let’s review that EMX has a large pipeline of earlier-stage and more advanced exploration and development project royalties that have a significant amount of growth potential for the future. This is a key area of royalty company’s discovery optionality (outside of the exploration upside on their existing producing projects), that gets little to no value from analysts or drive-by resource investors, but for the discerning value investor, this is a huge arbitrage in valuation to exploit.

So many investors really are not long-term investors, despite their claims otherwise, because they always want news catalysts immediately, want to see rapid growth through constant acquisitions, and typically only look at producing royalties to size up and compare royalty companies. This is such a colossal mistake and error in valuing these companies for the long-term and misses the forest for the trees…. Even if most of the well-established royalty companies, like EMX, did absolutely nothing for the next decade, they’d still have a pipeline of projects moving from advanced exploration to economic studies to development and then into production. Investors that regularly dismiss the pipeline of pre-revenue royalties in these companies do so at their own expense.

We should also flag the unique relationship between EMX Royalty and Franco-Nevada.

First of all, Franco-Nevada holds a 6% stake in EMX, and they don’t go around positioning in hardly any junior resource companies; (so that in itself is quite a statement).

Franco-Nevada has recently become the new sole lender to EMX Royalty, with the news announced June 20th, where EMX has borrowed a $35 million loan from FNV to repay the $34.66 million outstanding balance of the loan owed to Sprott Private Resource Lending II. As a shareholder, I liked seeing this news because the $35 million senior secured term loan facility doesn’t mature until July 1, 2029.

EMX Royalty and Franco-Nevada have jointly syndicated royalty purchases (e.g., Caserones) and are actively engaged in a joint venture seeking new royalty financing opportunities.

In addition to the synergistic partnership with Franco-Nevada, there are a host of other solid companies that EMX Royalty has as investors in their stock, as project operators, and as option partners.

Dave Cole, President and CEO of EMX Royalty Corp, joined me the end of last week over at the KE Report, for a comprehensive update on their distinguishing value proposition in the royalty space. We get updates on a number of their key copper, gold, and critical minerals partner projects, reflect on their revenue-generating pre-production royalties, review their Q1 financials, and strike the balance between further paying down debt in tandem with buying back Company shares.

EMX Royalty Corp – Multiplicative Optionality Across 170 Precious Metals And Critical Minerals Royalties – 06-27-2024

Thanks for reading and may you have prosperity in your trading and in life!

Shad