Opportunities With Mid-Tier And Junior Royalty Companies – Part 5

Excelsior Prosperity w/ Shad Marquitz – 06-03-2024

Welcome back to another update reviewing the opportunities in the mid-tier and junior royalty companies. In the first 4 articles in this series, we established the key value drivers, diversification advantages, risk mitigation advantages, and large net asset value per employee found in the royalty and streaming companies.

We also have previously highlighted the first 4 companies in this category:

Sandstorm Gold (SSL.TO) (SAND), Metalla Royalty & Streaming (TSX.V:MTA) (NYSE:MTA), Elemental Altus Royalties Corp. (TSXV: ELE) (OTCQX: ELEMF), and Vox Royalty Corp. (TSX: VOXR) (NASDAQ: VOXR).

Here is a link to [Part 1]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior

Here is a link to [Part 2]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-6b8

Here is a link to [Part 3]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-f34

Here is a link to [Part 4]:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-1e5

Here in [Part 5] of this series, we’re going to review some of the recent news from the first 4 companies covered, tease the 5th company we’ll take a deep dive on next time, and also introduce 2 new royalty and streaming companies not held in my personal portfolio, but that are key companies in the sector that we’ve recently interviewed over at the KE Report

So let’s get into it…

The first company we discussed in this series was Sandstorm Gold, and they’ve put out 2 key news releases last month in May.

Sandstorm Gold Royalties Announces 2024 First Quarter Results - May 2, 2024

https://www.sandstormgold.com/sandstorm-gold-royalties-announces-2024-first-quarter-results/

First Quarter Highlights [my comments in brackets]

Revenue of $42.8 million, Attributable gold equivalent ounces of 20,316 ounces, Cash flows from operating activities of $32.9 million, Record cash operating margins of $1,782 per attributable gold equivalent ounce

[those are pretty fat cash operating margins, but most categories were down compared to the first quarter of 2023, so I’ll be looking to see a stronger 2nd quarter out of Sandstorm]

The Company has continued to focus on de-levering its balance sheet and made $20 million in net repayments on its revolving credit facility during the first quarter.

[Sandstorm has been getting punished a bit for carrying higher debt levels on that credit facility, but when I spoke with Kim Bergen, Vice President of Capital Markets for Sandstorm Gold back in Q1 she mentioned that paying this down was going to be a big focus of the company over the next few quarters; so it is nice to see them making progress here]

· Sale of select non-core, non-precious metals assets: In May, the Company announced it had signed a definitive purchase agreement with Evolve Strategic Element Royalties Ltd. to sell a package of royalties (including Highland Valley Copper, Seymour Lake, and any future royalty proceeds exceeding $10 million from Copper Mountain) for cash consideration of $21.0 million. Upon completion of the Evolve Transaction, Sandstorm will have completed the sale of over $50 million of non-core royalty and equity investments since the third quarter of 2023, which includes cash consideration of approximately $40 million.

[Interesting to see a royalty company divesting “non-core” royalties, versus acquiring them, but part of their plan to keep rightsizing their balance sheet, and actually nice to see them trimming some of the fat. Of course, Evolve Strategic Element Royalties is purchasing them because they see value in the assets.]

· Renewal of Normal Course Issuer Bid: In conjunction with accelerated deleveraging driven by recent non-core asset sales and the current commodity price environment, Sandstorm announced in May that the Board of Directors has approved the use of the renewed Normal Course Issuer Bid, which allows the Company to purchase up to 20 million of its common shares from time to time when management believes the common shares are undervalued by the market.

[So they’ll be in there buying shares on pullbacks. It is good to see this, but the question also arises of if it is a better use of capital to buyback shares, or to put that money towards new transactions. Still this could be another value driver and underpin some supportive buying under any future selloffs in the stock.]

Sandstorm Gold Royalties Provides Asset Updates; Greenstone Pours First Gold - May 24, 2024

Equinox Gold Corp. (EQX) has announced first gold pour at its 100% owned Greenstone gold mine in Ontario, Canada. The inaugural gold pour was achieved on schedule, producing 1,800 ounces of gold from the full recovery circuit, with all equipment operating as expected.

[This is a big deal for Equinox, a big deal for Sandstorm, and a big deal for gold production in Canada. Very nice to see their company deliver the Greenstone mine on time and on budget, after a slew of Canadian mine cost overruns and backdated timelines like Argonaut’s Magino Mine, IAMGOLD’s Côté Lake Mine, and Ascot’s Premier Gold Mine]

[there were some other royalty partner updates on other projects embedded in this news that I’ll just quickly line item here, that folks can click on the above link to read more into them.]

Develop Global’s Woodlawn Production Restart Study Outlines Pre-Tax NPV of A$658 Million

Bonterra and Osisko Mining Announce Initial Exploration Results Under Urban-Barry Option Agreement

Endeavour Mining Corp’s Houndé Gold Mine Exploration Program Update

Lundin Gold’s Fruta del Norte Mineral Reserves Increase to 5.50 Million Ounces

METALLA REPORTS FINANCIAL RESULTS FOR THE FIRST QUARTER OF 2024 AND PROVIDES ASSET UPDATES - May 15, 2024

https://www.metallaroyalty.com/_resources/news/2024/MTA_NR_Q1_2024_Results.pdf

Brett Heath, President, and CEO of Metalla, commented, "In the first quarter of 2024 we focused on integrating and streamlining our business following the completion of the merger with Nova Royalty in December 2023. Now we will continue to seek acquisitions that will be accretive to shareholders and look for ways to refine our current portfolio of royalties to maximize value.”

• Received or accrued payments on 624 attributable Gold Equivalent Ounces (“GEOs”) at an average realized price of $2,069 and an average cash cost of $8 per attributable GEO

• Recognized revenue from royalty and stream interests, including fixed royalty payments, of $1.3 million, net loss of $1.7 million, and Adjusted EBITDA of $0.1 million

• Generated operating cash margin of $2,061 per attributable GEO from the Wharf, El Realito, Aranzazu, La Encantada, the New Luika Gold Mine stream held by Silverback Ltd. and other royalty interests

[It’s not a huge amount, the 624 gold equivalent ounces, but those are really hefty margins… still it’s a net loss for the quarter, and so looking to see more growth of GEOs to get them into a net positive situation as more mines come online over the next 12-18 months.]

The press release then goes on to outline a ton of royalty partner asset updates at:

First Majestic Silver’s La Encantada, Agnico Eagle’s El Realito & Fosterville & Amalgamated Kirkland & North AK & Wasamac & Akasaba West & Camflo & Detour DNA, Coeur Mining’s Wharf, Aura Minerals’ Aranzazu, Shanta Gold’s New Luika, IAMGOLD’s Côté-Gosselin, First Quantum’s Taca Taca, Polymetals Endeavor, G Mining Ventures Tocantinzinho, Equinox Gold’s Castle Mountain, Sierra Madre’s La Guitarra, St. Barbara’s Fifteen Mile Stream, and more…

[what really stands out to me is the quality of major mining operators, and also just how many royalties they have on Agnico Eagle’s portfolio of projects].

Elemental Altus Royalties Announces Record First Quarter Revenue - May 21, 2024

https://elementalaltus.com/elemental-altus-royalties-announces-record-first-quarter-revenue-2/

Highlights [Note the improvements year over year from Q1 of 2023]

Royalty revenue of US$3.3 million and adjusted revenue of US$4.7 million, up 24% on Q1 2023

Attributable Gold Equivalent Ounces (“GEOs”) of 2,283 ounces, up 13% on Q1 2023

Operating Cash Flow plus Caserones dividends of US$1.2 million, compared with a loss in Q1 2023 and expected to grow through 2024 as margins increase

Adjusted EBITDA of US$3.2 million, up 42% on Q1 2023

Diba remains on track to be the Company’s newest producing gold royalty. Allied Gold Corp (TSX: AAUC) have announced that mining is expected to commence in Q2 2024

Elemental Altus on course to meet guidance of 10,000 to 11,700 GEOs as production increases over the year. This guidance represents at its midpoint a 19% increase on 2023 and provides top-line exposure to gold and copper prices

Repaid US$5 million debt in Q1 2024, leaving US$25 million undrawn on the credit facility and with approximately US$9 million cash on quarter end prior to Q1 royalty receipts.

[All-around solid financial and operational quarter for Elemental Altus. It’s humming right along. I’m working to get an update with Fred soon over at the KE Report later in the week to dive into Q1 financials and a recent acquisition they announced, so stay tuned for that.]

Vox Announces Q1 2024 Financial Results and Declares Quarterly Dividend

- May 9, 2024

https://www.voxroyalty.com/_resources/news/nr-20240508.pdf

First Quarter 2024 Highlights

• Cash flows generated from operations of $1,212,154, up ~142% from $500,017 in Q1 2023.

• Cash and accounts receivable of $12,839,842, Working capital of $10,684,347

• On January 16, 2024, the Company entered into a definitive credit agreement with the Bank of Montreal providing for a $15 million secured revolving credit facility. The Facility includes an accordion feature which provides for an additional $10 million of availability subject to certain conditions.

• Revenue of $2,882,512 Gross profit of $2,414,139

• On March 7, 2024, increased quarterly cash dividend by 9.1% to $0.012 per common share

Vox Completes Acquisition of Strategic Australian Royalty Portfolio - 14 May 2024

https://www.voxroyalty.com/_resources/news/nr-20240514.pdf

Spencer Cole, Chief Investment Officer of Vox stated: “We are excited to complete this Australian royalty portfolio investment and we expect meaningful revenue from Castle Hill from early 2026 onwards. Of note, this transaction increases our large-cap operator portfolio weighting to over 65%, adding 3 assets operated by Australian gold producer Evolution Mining, who produced over 650,000 gold ounces and meaningful amounts of copper in the 2023 fiscal year. This portfolio also provides Vox investors with added copper, cobalt and rare earth metals exposure across the Halls Creek and Broken Hill royalties. Vox now owns over 50 separate Australian assets, the majority of which are benefiting from the ‘rising tide’ of record high AUD-denominated gold and copper prices.”

[I’ve been working to get a Vox update interview on the KE Report with Kyle or Spencer the last few weeks, but they’ve been out traveling and all over the place and we just haven’t been able to connect, but stay tuned for that sometime soon…]

OK, with those updates out of the way on the first 4 companies we’ve covered so far in this series, let me also tease that in [Part 6] of this series, we’ll be getting an updated interview over at the KE Report with Dave Cole of EMX Royalty Corp (TSX.V: EMX) (NSYE: EMX), and then taking a deep dive into that company and their recent Q1 Financials and acquisition newsflow.

For now, here is a somewhat recent interview we conducted with Dave back in February, that gives a nice snapshot of the company and key assets as a way to get acquainted or updated.

EMX Royalty – Value Proposition, Royalty Partner Updates, Paying Down Debt, & Buying Back Stock

Now, all 5 companies aforementioned are positions I hold in my personal portfolio, and Metalla, Elemental Altus, EMX, and Vox have been sponsors of the KE Report, so I’m biased in those regards.

However, just so readers here don’t think I only talk my book, we’re going to take a brief look at 2 other solid royalty companies that we’ve interviewed over at the KE Report that have good teams, compelling royalty and streaming assets, and are definitely other standout companies in the sector.

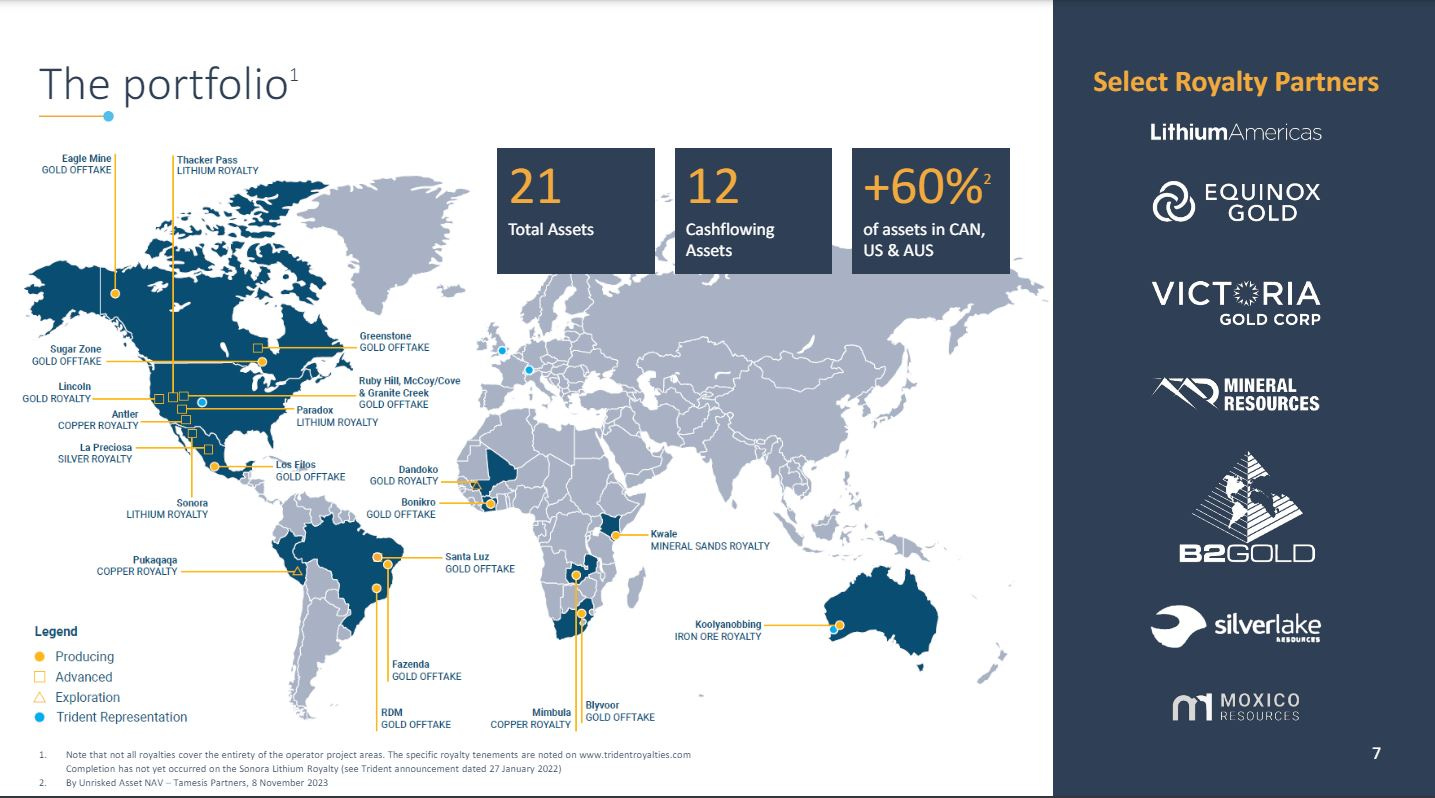

Trident Royalties – Q1 2024 Financial Recap, Growth Outlook Into Next Year

May 15, 2024

In this Daily Editorial we get an update from Trident Royalties (AIM:TRR – OTC:TDTRF). We recap the Q1 2024 financial results and look ahead to royalties and offtake agreements, within the Company’s portfolio, that are advancing toward cash-flow.

Adam Davidson, CEO and Executive Director, and Justin Anderson, VP Americas at Trident Royalties join us to prove the update. We focus on the key assets with the portfolio and the diversification across a range of metals. We discuss the Company’s cornerstone lithium asset, as well as the outlook for future acquisitions, especially outside of precious metals in a more diversified portfolio of commodities exposure.

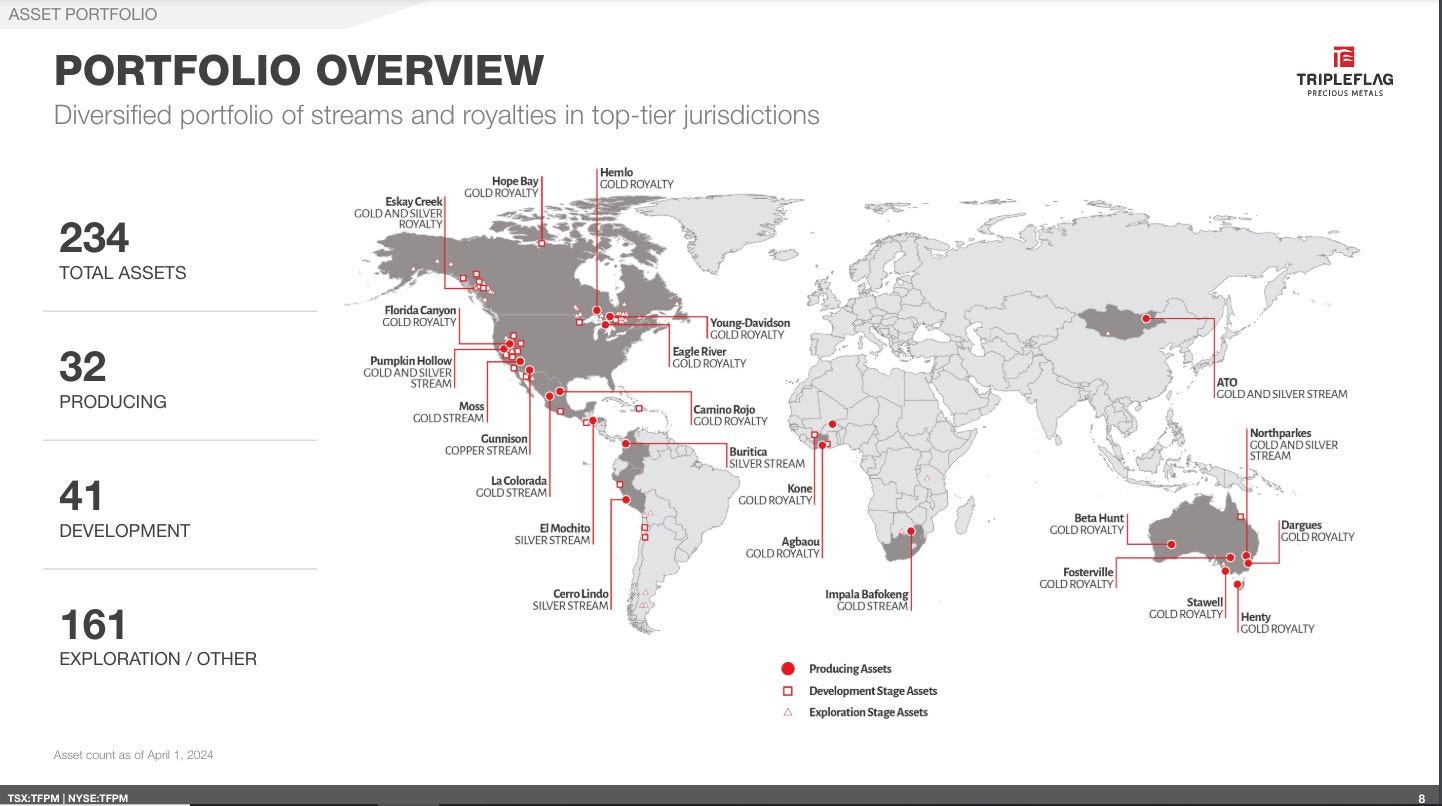

Triple Flag Precious Metals – 7 Consecutive Years Of Growth And Royalty Project Updates - Apr 16, 2024

Shaun Usmar, Founder, CEO, and Director of Triple Flag Precious Metals (TSX: TFPM) (NYSE: TFPM), joins us for an update on operations growth and royalty partners updates. Of their 234 total royalties and streams, there are 32 paying assets in production, 41 assets in development, and 161 assets at the exploration stage. We start off reviewing how the company has continued growing and diversifying since our conversation early last year, right after their acquisition of Maverix Metals (NYSE: MMX), and how they are approaching future accretive acquisitions and creating royalties with mining partners.

Shaun outlines that their portfolio achieved the seventh consecutive annual gold equivalent ounces (GEOs) record for Triple Flag and a compound annual growth rate in GEOs of more than 20% since 2017, while delivering 105,087 GEOs meeting their sales guidance for 2023. In 2024, the Company expects attributable royalty revenue and stream sales of 105,000 to 115,000 GEOs, and they are targeting a 5-year average moving forward of approximately 140,000 gold equivalent ounces from 2025 – 2029. Triple Flag PMs renewed their quarterly dividend of US$0.0525 per common share, and also renewed their normal course issuer bid to continue purchasing back shares of the Company.

We outline some of the key cornerstone assets in the portfolio of projects, such as the major contribution from the gold and silver streams on Northparkes and Cerro Lindo mines, or the cash-flowing producing royalties from Fosterville, Young-Davidson, RBPlat, Buritica, Beta Hunt, Camino Rojo, assets with a clear focus on precious metals in the Americas and Australia.

In addition to the strength of the operators for the 32 assets already in production, we discuss the how the Triple Flag team vets the upside optionality for exploration and development on their overall large basket of royalties and streams, in tandem with exposure to overall land packages to capture future growth and investment. Shaun outlines the extensive pipeline of growth projects including Hope Bay, Eskay Creek and Koné continued to advance down the development path.

That’s it for this [Part 5] in this evolving series on junior and mid-tier royalty and streaming companies, and there will be a number more of these articles on this topic in the weeks and months ahead. #GotRoyalties?

As always, thanks for reading and may you have prosperity in your trading and in life!

- Shad