Opportunities In Growth-Oriented Silver Producers – Part 11

Excelsior Prosperity w/ Shad Marquitz – (06/14/2025)

With the strength of silver breaking out of the $32-$34 channel and punching well up above $35 pricing resistance over the last couple weeks, there has been a lot of investor interest and positioning in the silver stocks.

In the near future on this channel, we are going to circle back to the gold stocks, royalty stocks, uranium stocks, copper stocks, and oil & gas stocks, but it’s been hard to ignore the allure of silver and the upside leverage it can provide when it really starts to get moving. As a result, we’re going to check in with a few of the junior silver producers, because we’ve had good news updates on their Q1 financials, and recently hosted a number of the management teams over at the KE Report to get updates on their operations.

James Anderson, CEO of Guanajuato Silver (TSX.V:GSVR) (OTCQX:GSVRF) mentioned several times in discussions at the Atlanta Top Shelf conference in mid-May, and in the recent interview we had together the end of last month that he really felt their company was at an important “inflection point.” Here’s that interview for anyone that missed it.

Guanajuato Silver – Solid Q1 2025 Financials Demonstrate The Company Is At A Strong Inflection Point

I’d agree with James with regards to G-Silver being on the precipice of breaking out from a balance sheet perspective, from operations efficiencies standpoint, and also from an exploration perspective… which in my estimation should lead to a big rerating in the stock over the next few quarters. {That’s not investment advice… just sharing my personal outlook and thesis}

NEWS UPDATE: Monday June 16th:

Guanajuato Silver Recognised for Social Responsibility in Mexico

“Guanajuato Silver Company Ltd. is pleased to announce it has received Mexico's Socially Responsible Enterprise certification, which recognizes the quality of the Company's community outreach and integration programs throughout 2024; and as previously announced on April 28, 2025, the Company confirms that the amended terms of its Gold Credit Facility with Ocean Partners UK Ltd. have been finalized.”

James Anderson, Chairman & CEO said, "The reduction of our monthly loan payments by over 200 ounces of gold per month provides the Company with improved financial flexibility as we pursue opportunities to grow our business at a time of increasing interest in precious metals."

Over the last couple months, everywhere I look though, it would seem that most of the smaller to mid-tier junior silver producers are also at key inflection points… whether it’s the emerging mid-tier producers like Santacruz Silver, Endeavour Silver, Americas Gold and Silver, or Avino Silver and Gold, or smaller producers like Impact Silver, Silver X, or Sierra Madre Gold and Silver.

The reasons for this inflection point may vary from company to company; from turning the corner in optimizing their operations, adding new equipment, ramping up production, building key development projects into mines, lowering overall costs, and pushing the exploration envelope with interesting drill programs.

It seems like a great time to check in with some of these portfolio positions both fundamentally and technically, on key news and recent charts, as well as giving readers of Excelsior Prosperity the opportunity to also hear directly from these management teams.

So, let’s get into it…

One of the silver producers that has really been on tear higher lately has been Santacruz Silver Mining Ltd. (TSXV: SCZ) (OTCQB: SCZMF); and for good reason. Their 2024 financials were quite impressive, and then their recently released Q1 financials were also equally eye-popping. Let’s have a look at those numbers:

Santacruz Silver Mining FY 2024 Highlights

Revenues of $283 million a 13% increase year-over-year.

Gross Profit of $57 million, a 1,670% increase year-over-year.

Net Income of $165 million, a 1,594% increase year-over-year.

Adjusted EBITDA of $53 million, a 200% increase year-over-year.

Cash and cash equivalents of $36 million, a 622% increase year-over-year.

Working Capital was $46 million at the end of FY 2024.

Cash cost per silver equivalent ounce sold of $21.90, a 16% increase year-over-year.

AISC per silver equivalent ounce sold of $26.01, a 15% increase year-over-year.

Silver Equivalent Ounces produced of 18,651,701, a 1% decrease year-over-year.

I’m continually amazed that a company that produced $283M in revenues and $165M in Net Income, and had production of 18.65 million ounces of silver equivalent for it’s annual metrics is still valued at $330M market cap. The market is not always right…

There have been peer companies (including the big 3 that were just acquired Gatos,SilverCrest, and MAG) but also Aya G&S, Endeavour, only producing 2.5-10 million ounces of silver equivalent for the last couple of years, in a backdrop of lower silver prices than we have today, that still garnered $1-$2B valuations.

Last year, before the Gatos acquisition, First Majestic produced 21.7 million AgEq ounces and was worth ~ $2.5B. (That’s only 3 million more AgEq oz than SCZ)

It seems to my mind that 18.65 million AgEq ounces from Santacruz Silver (when 48% of their production is directly from silver) should be valued in billions and not hundreds of millions… but that’s the kind of inefficient markets that we have at present. (So, are the markets always right? Not really…)

From my estimation, Santacruz Silver could go up 5x-7X from current levels, just to get valued more in line with peer companies… and that is if silver prices just channeled sideways in the mid $30s.

If we see silver punch up into the $40s then fuggetaboutit, as this stock will blast up leaving many investors chasing it higher, at least from my vantage point.

We covered that in more detail in the 2nd half of our initial article on Santacruz back in [Part 6] of this series on growth-oriented silver producers.

Fast-forward to Q1 2025 metrics for (SCZ.V) and there were more record financial metrics with 4-digit year-over-year comparables.

Q1 2025 Highlights

Revenues of $70.3 million, a 34% increase year-over-year.

Gross Profit of $27.9 million, a 6,882% increase year-over-year.

Adjusted EBITDA of $27.5 million, a 2,202% increase year-over-year.

Cash and cash equivalents of $32.5 million, a 706% increase year-over-year.

Working Capital of $51.7 million, a 7,530% increase year-over-year.

Cash cost per silver equivalent ounce sold ($/oz) of $17.84, a 16% decrease year-over-year.

AISC per silver equivalent ounce sold of $22.34, a 8% decrease year-over-year.

Silver Equivalent Ounces produced of 3,688,129, a 5% decrease year-over-year.

(if there is another silver company putting out larger year-over-year increases in revenues, gross profits, adjusted EBITDA, cash, or working capital then please email me about it as I’d like to buy them too) 😊

Arturo Préstamo Elizondo, Executive Chairman and CEO of Santacruz Silver Mining, joined me over at the KE Report yesterday, June 13th, to recap their key record Q1 2025 financial results along with a comprehensive review of all operations. Santacruz Silver operates 1 mine in Mexico, and 5 mines, 3 mills, and an ore feed-sourcing and metals trading business in Bolivia.

Santacruz Silver – Record Q1 2025 Financials and Comprehensive Operations Review In Mexico And Bolivia

One area I saw investors concerned about was the lower production in Q1 (3,688,129 silver equivalent ounces) compared to Q4 (4,710,013 silver equivalent ounces), so of course in comes all the F.U.D. (Fear, Uncertainty, and Doubt) about what is “going wrong,” but nothing could be further from the truth.

In the interview above, Arturo covered that the 1st quarter is always seasonally the weakest and Q4 is always the strongest, so the contrast is more noticeable. Q2 and Q3 will in all probability be up well over 4 million ounces of AgEq each, and then Q4 will likely be another blowout quarter in the higher 4.5+ million AgEq oz.

This is precisely why average herd investors get tripped up, because they extrapolate out the immediate past into perpetuity, and come to false assumptions.

Savvy investors do their homework to find out the “Why?” behind the numbers, and actually listen to the guidance from the companies. Then they can do a little reading between the lines to come up with their future expectations.

For Q1, there were also temporary water issues to deal with at Bolivar and those were resolved coming into Q2. I also saw monkey-chatter about their Zimapan mine being so much higher cost, and thus there were problems in paradise. Not at all… Zimapan was higher cost this quarter was because they just bought some new equipment to optimize operations (like 3 new Scoop trams that had to be reflected last quarter). They are investing in Zimapan to take advantage of the higher-grade 960 Level, which Arturo mentioned is setting them up for the next 20 years. Those were both one-off effects taken in Q1, but resolved for Q2 and moving forward for the balance of the year.

On the positive side operationally, there was better setup with San Lucas ore-feeding business absorbing the ore from the Reserva Mine to blend with ore from the small-scale miners. This meant it was not being blended with Tres Amigos and CQCQT which improved the metallurgy there, and this made Caballo Blanco much more efficient with better metals recoveries; as well as boosting the San Lucas operations improving efficiencies.

I didn’t see anybody taking swipes at the company that considered if they had such a blowout quarter financially in Q1, with lower overall AgEq production, and in taking on and resolving the 1-off water issue at the Bolivar mine, and in realizing the capital invested in Zimapan, then what do they think Q2 financials will look like with higher AgEq production and those aforementioned issues in the rear-view mirror?

My best guess is that Q2 is going to be an absolute blowout quarter for the company financially. They’ll have more production, lower All-In Sustaining Costs (AISC), a much higher average silver price, and they’ll have paid down even more of their early repayment of the Glencore loan. Skate to where the puck is going…

The other big overhang in this stock appears to be squeamish investor sentiment towards Bolivia. I’ve had 4 different people mention in the last 2 weeks they like some of these fundamentals, but struggle with the jurisdiction exposure. Then a handful of other people, that I otherwise respect, downright scoffed at mining in Bolivia. OK. So, let’s talk about that…

Sure, Bolivia has been more risky in the past, but not really that bad for the last 4-5 years... no more so than Mexico, Colombia, Peru, Chile, or Ecuador.

It’s not nearly as risky or anywhere close to the same ballpark as Guatemala, Panama, DRC, Burkina Faso, or Mali.

People that are domestic snobs, only extolling the virtues of investing in US and Canadian mining stocks, and that shun international projects in the rest of the world have missed so many opportunities over the years.

There are plenty of problematic areas inside Canada or the US...

First Nations issues and radically opposed environmental groups in Canada have stalled plenty of projects over the years.

In the USA, I’ve seen far more projects in Alaska (Northern Dynasty, Trilogy Metals, Constantine) have social license or permitting issues than I ever have in Bolivia. Minnesota has vast mineral wealth that’s been stalled for decades. New Mexico has had all kinds of issues with the Navajo and uranium miners.

So, this phobia of foreign locations or premiums for North American projects does need to be accounted for, and properly discounted, but still taken with a huge grain of salt.

With regards to jurisdictional risk, I see risks everywhere, as there are always opposition groups to mining, illegal mining operations that can have flare ups, the risk of government increased taxation or endless permitting risks all over the planet.

There are no 100% “safe” jurisdictions. Nevada, Wyoming, Alberta, and Saskatchewan are mostly safe, but it still depends on the local area and community always. Also bad management teams create issues in good areas.

British Columbia and Ontario are pretty good, but sometimes even they have either political permitting snags, or have seen their fair share of First Nations issues.

Idaho is pretty good, especially if a deposit is in the Silver Valley, but far from perfect outside of that area.

Texas is good for Uranium & Oil & Nat Gas, but there aren't many precious metals projects there of note.

Investors love to throw up the jurisdictional penalty card on anything outside of North America, but they leave so much money on the table… in West Africa, East Africa, South Africa, Central America, South America, Europe, and compelling parts of Asia as a result.

Case in point: So many investors have been paranoid about Nicaragua for years, and had a complete “freak out” when the US announced sanctions on Nicaragua back in late 2022. Some sold out of positions at exactly the wrong time, instead of buying into that media-induced F.U.D. that got echoed throughout the resource sector by the uninformed.

In my personal portfolio, 2 of the positions where I got 3-4 baggers the last couple of years have been with Calibre Mining and Mako Mining, both primarily operating smack in the heart of Nicaragua.

We had both companies on the KE Report back at the time of all the nail biting in 2022, and they outlined that they are Canadian companies that have been operating in-country for many years now, and those sanctions had little to no impact on them.

So again, intelligent investors get information and don’t fall for emotional and misguided media hype. Sure, there is always risk that Canada could place sanctions on Nicaragua, but that also never happened. Did that risk really outweigh the operational excellence of Calibre and Mako the last few years? (Clearly it did not and investors shunning that jurisdiction missed huge gains)

I know of 3 junior operating companies in Bolivia - Santacruz Silver, Andean Precious Metals, and the private company San Cristobal (operated by the Crescat Capital guys). All of them have been operating for a couple of years now, and none have had any big problems. Then there are the 2 advanced explorers/developers, New Pacific Metals and Eloro Resources, and neither of them have had any problems to my knowledge.

The Potosí area of Bolivia has had silver, zinc, and tin mining going on for hundreds of years now, and it is part of the fabric of the culture… just like in much of Latin America. So Bolivia gets a bad wrap, but it's not been nearly as challenging as Mexico has the last few years, and I've still got lots of exposure to Mexico. So yes, it's risky,…but so is almost everywhere else.

With Santacruz, I find their valuation so mismatched compared to other mid-tier silver producers, that it's been one of my heaviest weighted positions for years and has been my largest position so far this year. My speculation is that it still will keep rerating higher when Q2 and Q3 and Q4 numbers roll in this year and overcome any perceived risks from Bolivia. It's not without risk though... but there is no jurisdiction or mining company without risk.

Technically, the chart for (SCZ.V) has been starting to wake up this year:

Pricing did really run up fast, doubling in price from May from the mid $0.50s to up over a $1.00 in a few weeks, so it got overbought on the RSI up near 88.

The recent pullback was likely from some more short-term traders pulling profits on a big rip higher in the stock. (In full disclosure I trimmed back 7% of my position into that recent overbought condition last week, but will also be looking to repurchase that if we see any more weakness in the share-price in the near-term).

There also may have been some concerns from the herds dithering over the lower Q1 production numbers (which we already addressed is seasonal and happens each Q1, for those paying attention to last couple years).

In the big picture analysis, their current $330Million market capitalization is still comically low for this mid-tier silver producer and I could see it easily going up 5x-7x from here.

If it becomes a $6-$7 stock with over a $2Billion market cap, then I’ll personally consider it more fully valued. {not investment advice… just sharing my personal thesis}

Let’s shift over to another growth-oriented silver producer that appears to be at an inflection point after putting out their Q1 financials and operations; Impact Silver (TSX.V:IPT) (OTCQB:ISVLF). Now this is a much smaller company and production profile than Santacruz Silver, but it also has a tiny market cap of CAD$72Million. It has much more torque to exploration than most of these silver producers; so I consider it hybrid company: part producer / part advanced explorer.

We first covered this stock back in [Part 4] of this series for anyone that needs a quick primer on it:

2024 was a tough year for the company due to the accounting treatment of the purchase of their Plomosas Zinc-Silver-Lead Mine in Mexico, but they got it profitable by Q4. Additionally, they changed their accounting process to be more compatible to how it’s done in the US and wrote off exploration as an incurred expense, instead of being capitalized like it had in the past, which changed the balance sheet in a disproportionate way for last year. However, they did clean up their balance sheet by the end of the year and ended the year with $9 million in working capital, $7 million in cash, and they still have no debt, which I find to be a huge plus.

Upon their Q1 financials being announced in late May, the Company reported revenue of $10.7 million for Q1 2025, more than double the $5.3 million reported in Q1 2024. This significant increase was driven by the commencement of new production at the Plomosas mine and higher commodity prices. EBITDA for Q1 2025 was $1.0 million, marking a strong recovery from the negative $3.6 million in Q1 2024. Net loss for the quarter was $0.1 million, a notable improvement compared to the net loss of $4.4 million in the same period last year. This reflects a substantial year-over-year improvement, as inflationary pressures on costs eased and commodity prices remained strong, supported by a higher aggregate production volume. At quarter-end, the Company had $6.6 million in cash and no structured debt.

Impact Silver Announces Q1 2025 Financial Results with Near Doubling of Revenue & Positive EBITDA of $1.0 MILLION

Fred Davidson, President and CEO of Impact Silver, joined me over at the KE Report on June 6th, to outline the key takeaways from the Q1 2025 financial and operations, and provides an update on the current production and exploration upside at the Zacualpan Silver-Gold District, as well as the Plomosas Zinc-Lead-Silver Mine in Chihuahua, Mexico.

Impact Silver – Review Of Q1 2025 Financials, Operations, and Exploration Initiatives At Both The Plomosas and Zacualpan Mines And District-Scale Land Packages

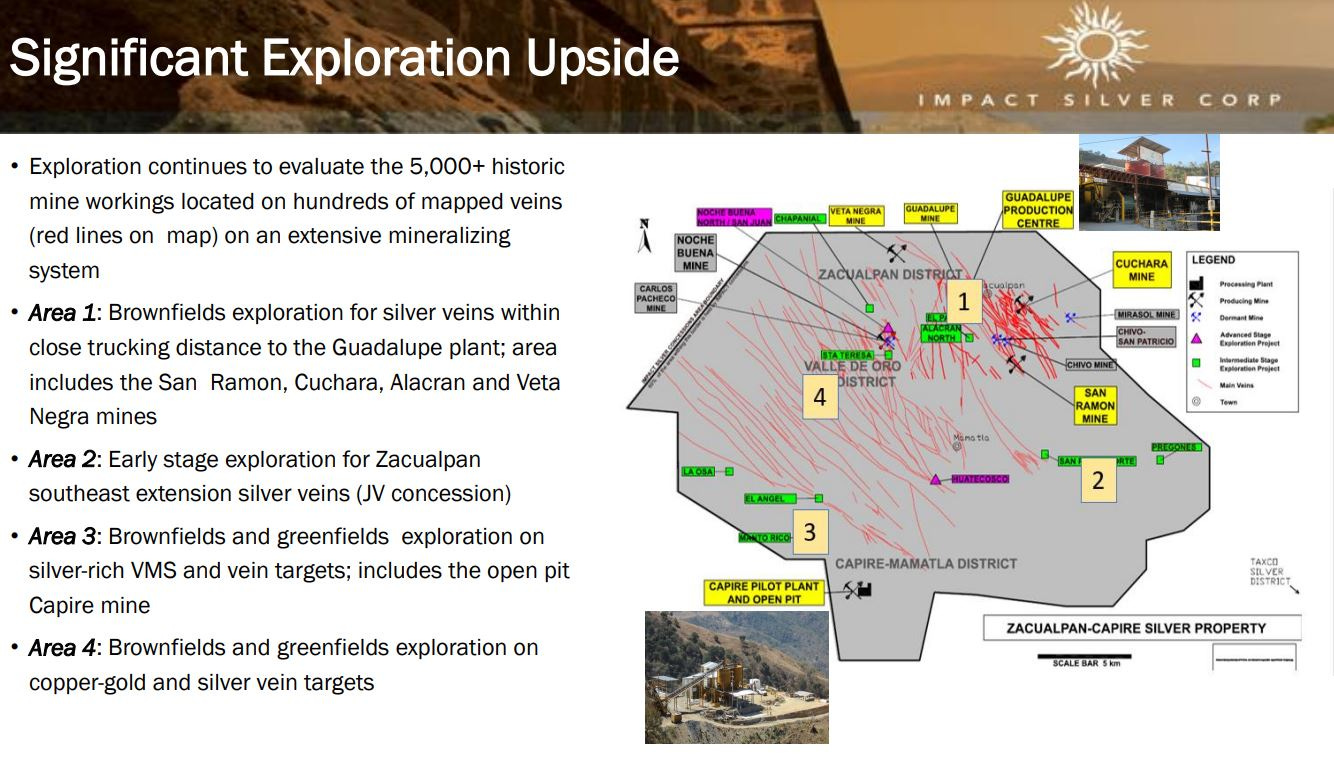

So the producing operations are chugging right along, but truth be told, I’m more animated personally by their exploration upside across their massive land package in Mexico. Drill results can still move the needle for this silver junior.

With regards to all the exploration initiatives for this year, we kicked things off in that discussion above with opportunities to keep exploring deeper underground for more high-grade zinc, lead, and silver at the Plomosas Mine.

Fred also points out that there is a new area of interest nearby that is more endowed with gold and copper mineralization, and that will be getting some upcoming surface drilling.

Shifting over to the Zacualpan Silver-Gold District the Company has 4 underground mines and 1 open-pit mine all feeding into the Guadalupe processing plant. Fred and I reviewed exploration targets at the new Kena Discovery at the Guadalupe Mine, the San Ramon Deeps and San Ramon South area at the San Ramon Mine, both a gold-rich and a silver-rich vein respectively at the Alacran Mine, some silver targets like San Antonio at the Mina Grande Mine, and a few target like Carlos Pacheco and Chapanial at the Valley de Oro exploration area.

There also was a lot of grumbling from the retail investing peanut gallery regarding their recent capital raise. Uninformed people (like usual) started weaving narratives of potential problems at the companies operations, or else they wouldn’t have needed to raise. Right? (Wrong)

This was total B.S., so we wrapped up our discussion where Fred outlined that the true purpose of the recent $5million capital raise is to accelerate all this exploration efforts at both district-scale properties, looking for areas to exploit with mining, and eventually growth in their production profile.

There is only so much exploration that they can fund out of existing operations, and they really want to step on the gas pedal and really gear up their exploration, so they are supplementing their normal exploration with a more beefed up program for this year. The value creation could really outweigh the dilution.

Like Guanajuato and Santacruz Silver, the technical daily pricing chart for Impact Silver is just now starting to wake up and get a little life in it from May into June.

One more brand new junior silver producer to squeeze in here, that is also at an important inflection point is Sierra Madre Gold and Silver Ltd. (TSXV: SM) (OTCQX: SMDRF). We had initially covered this stock in [Part 5] in this series, and here is that link for anyone that wants a quick primer on this company.

The market had been awaiting the Q1 financials, as it was really the first quarter of commercial production, and so far it was a solid start at their La Guitarra Mine.

Sierra Madre Announces Positive Q1 2025 Financial Results

- May. 07, 2025

https://sierramadregoldandsilver.com/read/auto-news-1746652099

Q1 2025 Highlights

Net Revenues: Silver revenues for the quarter totalled $2.34 million ($31.13 per ounce) and gold revenues totalled $2.89 million ($2,828 per ounce).

The Company sold 75,137 ounces of silver (“Ag”) and 1,022 ounces of gold (“Au”) or 165,093 silver equivalent (“AgEq”) ounces, based on the ratio of Au and Ag prices realized for each shipment in the period.

Cost of sales was $3.6 million, approximately $21.84 per AgEq ounce sold.

All-in-sustaining costs per AgEq ounce sold of $28.98 per ounce, compared to $32.18 in Q4 2024.

Gross Profit was $1.2 million.

Cash provided by operating activities was $535,000.

Current assets, including cash, totaled $4.3 million at March 31, 2025, up from $3.5 million in Q4 2024.

Q1 2025 Operational Details

Mine Operations: Milled 39,167 tonnes of material, silver recoveries averaged 79.21% while gold recoveries averaged 78.77%.

Production: Produced 70,176 ounces of silver and 1,001 ounces of gold.

Coloso Mining: On April 29 2025, Sierra Madre announced the start of underground mining at the Coloso mine within the Guitarra Complex. The estimated resource grades at Coloso are significantly higher in both silver and gold compared to the Guitarra mine veins. During the ramp up of Coloso mining, various blending percentages for mill feed will be tested to ascertain best recovery procedures. (so there you go… Mine #2 is already gearing up)

Alex Langer, President and CEO of Sierra Madre Gold And Silver, joined me last week on the KE Report to review the Q1 2025 operations and financial metrics showing profitability from the very first quarter of commercial production at the La Guitarra Mine and processing plant, in Mexico. We also highlight a number of future development and exploration value drivers for the Company across their district-scale land package containing 8 historically producing mines.

Alex then lays out the envisioned plan is to run the mill at 500 tpd most of this year, at the slated commercial production throughput. However, he then also shares the pathway forward where a modest amount of equipment can be purchased and installed to grow the mill throughput to 650 TPD by early 2026 (maybe even by later 2025), and then all the way up to 1,000+ TPD by the end of 2027. In addition to the potential of growth through production, we also discuss the leverage that a silver and gold producer like Sierra Madre will have to the potential of rising metals prices in 2025 and 2026.

Next we shift over into the larger growth vision of the company, as it will turn it’s focus to exploring this district scale land package the end of next year, funded through organically generated revenues.

The property hosts 8 different past-producing mines, with the first 2 priorities being to explore around the historic El Rincon and Mina de Agua mines.

Additionally, there is a non-compliant 17 million ounce historic resource at the Nazareno Mine, and also solid underground infrastructure connected to the nearby high-grade Coloso Mine, that First Majestic had put quite a bit of sunk cost into already.

Moving the Coloso Mine back into production will be another near-term area of future expansion, which will now see supplementary production complimenting the current production coming out of La Guitarra here in the last few weeks of Q2, but more importantly in Q3 and Q4.

Looking at the Sierra Madre 1-year daily chart we see a steady climb higher that has matched their milestones as they steadily have ramped up into commercial production this year.

Thanks for reading and may you have prosperity in your trading and in life!

Shad