Opportunities With Growth-Oriented Gold Producers – Part 2

Last Friday’s article highlighted the big opportunity still seen in the growth-oriented producers for the coming bull market cycle setting up to unfold in the year to come. It was more general in nature about the key takeaways, but then unpacked a few ideas at the end of the piece, with a specific example highlighted using i-80 Gold Corp (IAUX) (IAU.TO).

Here is a link to that primer and Part 1 introduction to some of the investing concepts around ‘growth-oriented gold producers.”

https://excelsiorprosperity.substack.com/p/opportunities-with-growth-oriented

In Part 2 of this series, now that the basic concepts have been established, my plan is to put a little more color around some of the specific opportunities and fundamental value drivers that I see in some more of the smaller and mid-tier growth-oriented gold producers. This growth is typically fueled by higher throughput or higher-grade, and is the result of solid development and exploration work. This type of solid value-creation work should provide these types of companies significant alpha in the unfolding PM bull.

For the sake of digesting the information, but not running on too long, I’ll likely just handle 2-3 companies in each of these updates. However, I have a lot to say about the company highlighted in this article; so this will be a more detailed single company update in this sub-sector of the gold stocks.

In Part 1 of this series, a list was provided, (also included down below) of some of the gold companies that I personally hold in my portfolio and see as being included in this “growth-oriented gold producer” category. Most of these companies are also in the “holy grail” category, because in addition to production growth on tap, they have also shown compelling exploration and development upside at various projects in their portfolio.

- Equinox Gold (EQX.TO) (EQX)

- Karora Resources (KRR.TO) (KRRGF)

- Calibre Mining (CXB.TO) (CXBMF)

- I-80 Gold Corp (IAU.TO) (IAUX)

- Argonaut Gold (AR.TO) (ARNGF)

- Orezone Gold (ORE.TO) (ORZCF)

- Thor Explorations (THX.V) (THXPF)

- Mako Mining (MKO.V) (MAKOF)

- Minera Alamos (MAI.V) (MAIFF)

- Lion One Metals (LIO.V) (LOMLF)* I’m including this earlier stage gold producer that is just starting to ramp up towards commercial production in 2024 in this list of companies because of the phased approach they are going to take to increasing their mill and production output over the next 2-3 years, in tandem with aggressive gold exploration at depth and across their 7km land package across a whole volcanic caldera in Fiji.

In future updates we’ll definitely be touching on even more of these stocks, and then eventually we’ll toggle over to some thoughts on the growth-oriented silver producers… but one step at a time.

For now let’s get to it, and we will focus this update and overview on Calibre Mining.

__________________________________________________________________________

As mentioned in the first primer article, some of my highest conviction plays, investing in the precious metals stocks, tend to be revenue-generating companies that can monetize higher metals prices through their production and expanding margins, and then reinvest those revenues into further growing their business.

Calibre Mining (CXB.TO) (CXBMF) is one of these types of growth-oriented gold producing companies that I personally hold in my portfolio. For full disclosure, over at the KE Report, we also follow Calibre as one of our site’s sponsor companies, so in those regards I’m biased towards this company.

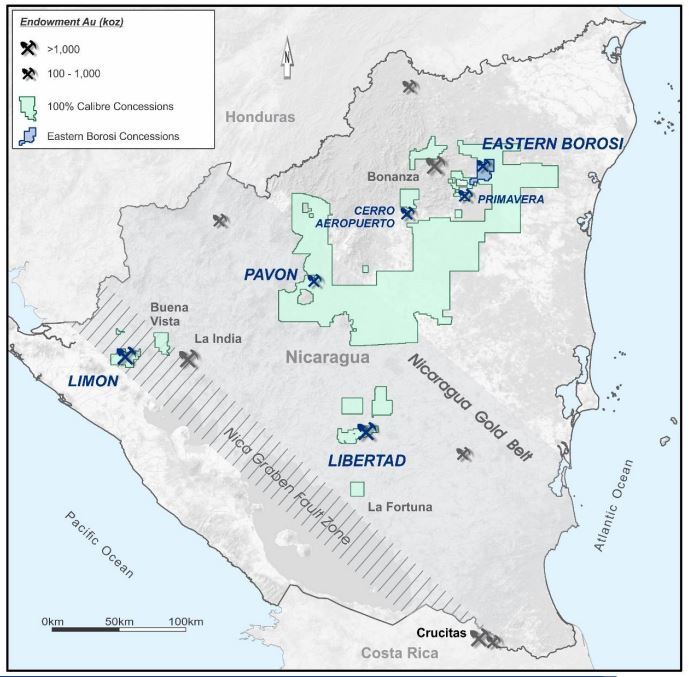

In addition to personally trading the technical price action of this company for a few years now, additionally at the KER we regularly conduct interviews with Ryan King, Senior VP of Corporate Development and IR at Calibre Mining. This has allowed me to stay up to date on the company newsflow and key developments, and to track their quarter over quarter operational and exploration progress in Nicaragua, Nevada, Washington, and soon the addition of Newfoundland.

What has continually impressed me with the Calibre Mining team, over the last few years, is their 2-pronged approach to growth:

1) They’ve continued to grow their resources at various projects through very aggressive exploration year after year, (often much more expansive and larger drill programs than most of the penny dreadful exploration plays that animate so many retail investors).

2) They’ve truly executed on production expansion by utilizing the “hub and spoke” development strategy at their primary mining operations in Nicaragua. It should be noted that they’ve also started to replicate this same successful existing mine optimization and expansion through exploration at their Pan Mine, and potential future spoke of development and production from the nearby Gold Rock Project in Nevada (which we’ll get to a little bit later).

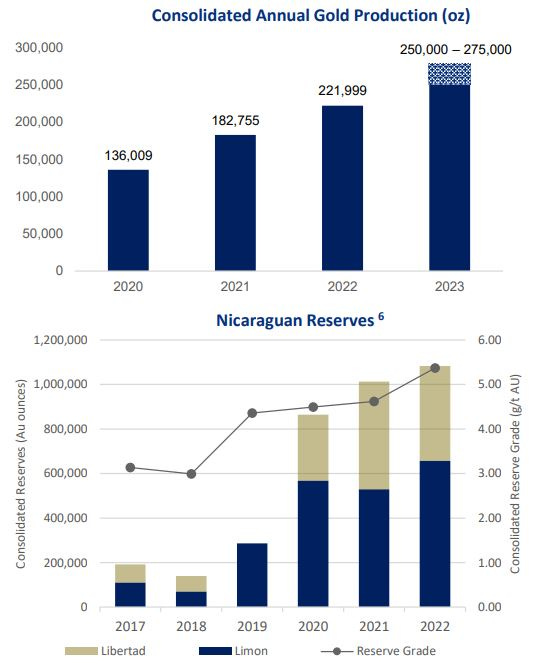

Sticking with their Nicaraguan operations, in the last few years they have excelled in discovering, developing, and then exploiting new satellite pits as “spokes,” and then trucking the ore from these new mines over to feed this into their Limon and Libertad Mills or “hub.” In this sense, they have undeniably executed on this hub and spoke method, and continue to find new areas of interest to build out even more spokes throughout their large land package and exploration concessions.

Many development-stage companies or single asset producers give this hub & spoke methodology a great deal of lip service, but in practice most companies rarely get more than one spoke going before running into challenges. In the time I’ve been following Calibre they’ve gone from one spoke, to two, and now three (with even more in development), all funneling in ore to their mills to continue feeding the beast.

Grade-Driven Growth:

It is also key to note that the hub & spoke strategy hasn’t just been trucking more of the same grade ore to their mills, but rather these new satellite pits like Pavon Central and Eastern Borosi have been much higher-grade (essentially double the average grade of material mined from 2019 to 2022). They have been able to put higher-grade gold ore and overall higher ore throughput into their mill to grow their production profile in 2023, and are set up to keep doing so in 2024.

Ryan King and I had a great conversation in early July about commencing production a their 2 new mines, where he really expands on this grade-driven growth strategy for Calibre Mining. We start off discussing why the high-grade gold ore now being mined at both the Eastern Borosi and the Pavon Central productions centers further substantiates that their hub-and-spoke mining strategy and is continuing to add much higher-grade ore through the Libertad Mill. Ryan outlines the pattern of year over year grade-driven growth from the Company.

Here is a link to that interview that still has a great deal of relevant information on this part of their business strategy.

https://www.kereport.com/2023/07/03/calibre-mining-commencement-of-eastern-borosi-production-center-bringing-in-more-grade-driven-growth/

Pavon is 300 kilometers away from the Libertad mill whereas their initial mine was more nearby the mill. It is a legitimate satellite pit. They first developed Pavon Norte 2 years back, and then Pavon Central was a whole new mining pit they dug out and started producing from in 2023. This area is now a solid second spoke.

Then Eastern Borosi was a totally new discovery, that went all the way from exploration to development and now production this year, and it is being trucked about 400 kms to the Liberatad Mill. So again, it’s a legitimate new mine and shows the CXB team continues to deliver with yet another satellite spoke.

Let’s Talk About The Management Team:

Many of the talking heads in the resource sector camp out repeatedly on the importance of seeking out a quality management team and board of directors for any company they are flagging. We hear this so often, but every single company out of the over thousand resource companies claims they have that “quality management team.” While I agree wholeheartedly that a strong managing team is crucial; what actually matters most to me is a given company team that is matched correctly with the job at hand and for delivering on their aspirations and business strategy. I want to see any team set a reasonable business plan and offer legitimate guidance, and then go out and achieve this plan. Sadly, most companies fail to do so in practice.

Unfortunately, a large portion of the companies in the resource sector (even ones we have been told repeatedly are led at the helm by the dream team) end of failing at their initiatives for a whole host of reasons and challenges that can upset the applecart in the mining business. So, when everything is distilled down, I care much less about most of the supposed highly compensated and touted superstars or legends, (that all have checkered histories of wins and losses, but people only promote their wins), and instead I give much more weighting to a management and operations team that really works well together to consistently under-promise and then they outperform.

The Calibre management team has done that in spades for several years in a row, and have hit or exceeded the vast majority of their milestones and guidance, just like they messaged to the market that they would. In contrast, I’ve watched other supposedly superior teams at other companies struggle to keep costs down, or fail to grow resources and reserves, or slip in increasing their production profile. So one thing to point out is that suggesting a management team or board is “high quality” is very, very, subjective in nature. The company results and execution, especially in tough markets, speak much louder than empty words and platitudes.

____________________________________________________________________________

The Calibre team has shown for the last few years that they are capable new mine builders, as well as existing mine optimizers. We are just now wrapping up the 4th quarter of 2023, so we won’t have all the figures in on Q4 or the full year for a couple months, but we can quickly look at the key metrics from Q3 and year-to-date figures press released to the market on November 7th.

Q3 2023 Highlights

Record cash on hand of $97 million, a 26% increase over Q2 2023 and 72% higher than the beginning of 2023;

Free Cash Flow increased over Q2, 2023 to $16.3 million;

4th consecutive record quarterly gold sales of 73,241 ounces grossing $143.9 million total revenue, at an average realized gold price of $1,929/oz;

Consolidated Total Cash Costs of $1,007 and All-in Sustaining Costs (“AISC”) of $1,115 per ounce;

Net income of $23.4 million or $0.05 per basic share;

Adjusted net income of $24.5 million or $0.05 per basic share;

Exploration success at Libertad yielded an Initial Mineral Resource Estimate at the Volcan Gold Deposit;

Intercepted high-grade gold targets at the Jabali Mine, potentially expanding resources;

Continued to expand zones of high-grade gold mineralization at Atravesada and along the VTEM gold corridor, both within the Limon Mine Complex;

High-grade, near surface drill results immediately north and south of the operating Pan Mine, demonstrate potential to increase resources, grade, and confidence across the property; and

Back in October, Ryan & I spoke again, where he provided a recap of these Q3 and year to date operation and production results in Nicaragua and Nevada, as well as an overall development and exploration update. While the production numbers were very strong, my key takeaway from this recent interview was more so about all the solid exploration work going on at multiple targets and projects, tying into the growth-oriented theme here.

We reviewed the continued exploration success at a number of drill targets and new areas of focus near their Libertad processing facility, especially at the Cerro Volcan Gold Deposit, which had recent news out about its initial open pit Mineral Resource Estimate five kilometers from their mill. We then pivoted over to more recently announced drill results from the expansion and infill drilling program at the high-grade Atravesada underground deposit located within the Limon Mine Complex; 2 kilometers west of the Limon processing plant. These high-grade intercepts continue to demonstrate the resource expansion potential at the Limon Mine complex. Many of the exploration targets and success with the drill bit the last 2 years has been guided by the VTEM data, and what they have dubbed the “VTEM Gold Corridor.”

We wrapped up this interview with a deeper dive into the Nevada operations and exploration upside around the Pan Gold Mine, as well as further exploration and technical studies underway at the Goldrock Project for the optimal pathway to development.

Here is a link to this interview from back in October on Q3 Operations and Exploration:

_________________________________________________________________________

Holy Grail Growth-Oriented Producers Have A Big Focus On Exploration Upside:

As already eluded to, the final piece in a company becoming a “Holy Grail Growth-Oriented Producer” is when a company with revenues, can then fund part of or all of it’s exploration through the ATM machine of it’s mine or mines. This self-funded exploration can thus expand the company resources, leading to either increasing production output or extending the mine life, without the accompanying dilution that plagues pre-revenue companies.

Most of the producers on my larger sector watchlists are not nearly as aggressive with exploration as Calibre Mining has been the last few years. In fact there are some producers doing surprisingly very little if any exploration, with the model for these companies being them preferring to replace ounces through acquisitions and mergers.

In that prior interview from October that was linked above, anyone listening would have noted that the whole second half of the discussion, after the operations report, was totally focused on just how much exploration and how many multiple drill rigs were turning all throughout Nevada and Nicaragua. When Ryan and I finished up that interview, we laughed off-mic that we still didn’t get to so much of the exploration work going on throughout their land package, due to time constraints. We both agreed to get back together in a month to get even more granular on all the ongoing exploration work, and that is what we did.

Synchronistically, on October 31st, the company had press released even more exploration results from the successful drilling around the Jabali Underground Mine area and other scout and resource drilling within and nearby the Libertad Mine complex. Mineral Resource grades at Jabali average 4 g/t gold historically, so the higher-grade drill results coming back at depth from underground drilling, approximately 100 meters below the main Jabali resource, confirmed that mineralization and continuity down-dip with strong potential for resource expansion.

Highlights at the Jabali Underground Mine include:

10.80 g/t Au over 14.3 metres Estimated True Width (ETW) including 26.72 g/t Au over 4.5 metres ETW in Hole JB-23-538A

18.84 g/t Au over 3.1 metres ETW including 31.30 g/t Au over 1.8 metres ETW in Hole JB-23-539

4.51 g/t Au over 3.1 metres ETW including 9.04 g/t Au over 1.5 metres ETW in Hole JB-23-540

8.44 g/t Au over 8.9 metres ETW including 22.08 g/t Au over 3.0 metres ETW in Hole JB-23-541

Some of the new areas of focus Ryan highlighted in this next interview together are near their Libertad processing facility, and we reviewed the continued exploration success at a number of scout drill targets along the same trend as the recently announced Cerro Volcan Gold Deposit open pit resource. These results demonstrate the strong potential to continue expanding resources and to discover new zones. Scout level drilling across the property has identified three new target areas located within 10 km of the Libertad mill at the Calvario, Salvadorita, Mestiza vein systems.

Highlights from the scout level drill program include:

14.39 g/t Au over 2.3 metres ETW including 48.91 g/t Au over 1.2 metres ETW in Hole CV-23-022;

32.84 g/t Au over 2.1 metres ETW in Hole CV-23-032;

17.40 g/t Au over 1.2 metres ETW in Hole CV-23-023;

156.7 g/t Au over 0.44 metres ETW in Hole SAL-23-004;

9.65 g/t Au over 2.1 metres ETW including 20.00 g/t Au over 0.8 metres ETW in Hole VN-23-137;

Additionally, we pivoted over to more recently announced drill results from the expansion and infill drilling program at the high-grade Atravesada underground deposit located within the Limon Mine Complex; 2 kilometers west of the Limon processing plant. These high-grade intercepts continue to demonstrate the resource expansion potential at the Limon Mine complex. Many of the exploration targets and success with the drill bit the last 2 years has been guided by the VTEM data, and what they have dubbed the “VTEM Gold Corridor.” This all ties into the continued theme from the exploration work at Calibre Mining of grade-driven growth.

Calibre Mining – More High-Grade Drill Results Returned from the Jabali Underground Drilling And Nearby Scout Drilling

______________________________________________________________________

Growing Through Acquisition Transactions:

Another option for more value creation with resource producers is to additionally grow through acquisitions. This involves looking for accretive transactions to pick up other producing or development-stage projects from other distressed companies, or simply non-core projects to larger companies. For some producers, not focused on exploration, this is their only means to grow resources and reserves. For Calibre it is just the icing on the cake…

In addition to the organic production grade-driven growth from Calibre’s hub and spoke strategy, and all the organic exploration and development potential ongoing in both Nicaragua, Nevada, and even some on Washington this year (they have 2 million ounces of gold at their Golden Eagle project and put out some more high-grade hits earlier this year), they are also now growing through acquisition. On November 13th, CXB surprised markets, and your author here too, with an announcement of one of these strategic M&A transactions. The Company announced that it has entered into a definitive arrangement agreement whereby Calibre will acquire all of the issued and outstanding common shares of Marathon Gold (TSX: MOZ – OTC: MGDPF ) pursuant to a court-approved plan of arrangement.

Key highlights of the Transaction include:

Creates a high-margin, cash flow focused, mid-tier gold producer in the Americas with estimated annual production of 500 koz Au per year (2025 – 2026E average)

Strong balance sheet with estimated combined cash of approximately US$148 million and significant free cash flow generation, ensuring the seamless completion of Valentine during the final 50% of construction

Significant combined mineral endowment of over 4.0 million ounces of mineral reserves, 8.6 million ounces of measured and indicated mineral resources (inclusive of mineral reserves) and 4.0 million ounces of inferred mineral resources (as further detailed in the tables below)3

Peer leading production growth of 80% (2024 – 2026E)

Approximately 60% NAV in tier-1 mining jurisdictions1 with pro-forma market capitalization of approximately US$750 million, providing scale, enhanced trading liquidity, and a strong re-rating potential as a mid-tier gold producer

Valentine to add expected average annual gold production of 195 koz at low projected All-in Sustaining Costs (AISC) of US$1,007 per ounce through the first 12 years of production beginning in 2025

Robust annual cash flow from operations of US$380 million (2025 – 2026E)

A continuous flow of exciting discovery and resource-building drill results from Nicaragua, Nevada, Washington, and now Newfoundland & Labrador

Of course, after digesting this news and hearing other voices in the sector opine on this deal, it was time to circle back up with Ryan for an update on the actual strategy and thought process behind this ongoing business combination between Calibre Mining and Marathon Gold. In the interview we just released last Friday on December 22nd, we get into some of the main value drivers of the pro-forma company, the opportunities for growth and value creation, the diversification of jurisdiction risk, and the quality of the management teams to move the Valentine Gold Project forward into production.

We also had Ryan give us a brief update on the closing of the previously announced C$40 million financing of Marathon, and that effective, after the closing of the Private Placement, Calibre owns 14.2% of the issued and outstanding Marathon Shares.

Calibre Mining – Unpacking The Proposed Business Acquisition Of Marathon Gold

Clearly though, this Valentine Gold Mine is an order of magnitude larger mine to bring into production, than the other smaller mines the CXB team has done up until present in this company vehicle. Having said that, the team at Calibre (Darren in particular) has brought online much larger mines with some of the majors he’s worked for in the past, so this is within their wheelhouse of experience. It will be interesting to see how the transition from the Marathon team to the Calibre team goes as far as better execution on bringing this into production in 2025.

Additionally Ryan has discussed a number of times on prior interviews that Darren and some of the management team have built very large mines prior to being with Calibre. Darren was very involved with some of the previous projects built for majors like Newmarket Gold which has taken over by Kirkland Lake, along with a number of mines for Newmont. Those prior projects had mines and mills developed and then were built to move into production on a scale more on par with the Valentine Gold project, so this is not this management team’s first rodeo.

Personally, I think the element of risk and wildcard that remains is they are taking over a project that is presently only half-way built , and a lot capital has already been deployed, with a lot left to deploy from their credit facility, from the $40 million just injected in the financing, through cash on hand at Calibre, and through incoming production revenues from CXB’s current mines.

Whether the baton pass and transition to the 2nd half of the mine build goes smoothly remains to be seen, but I’ve got a fair bit of confidence in the proficiency that the Calibre team has shown the last few years in both Nicaragua and Nevada. Of course, mining is a very tough business and riddled with challenges and potential choke points in operations, so it isn’t easy for any company. I just have seen them repeatedly deliver on projections, guidance, and milestones for a few years now and that gives me more confidence in a team that has consistently executed.

For all the reasons outlined above, Calibre Mining, remains one of my personal favorites and heavier-weighted positions as it relates to growth-oriented gold producers.

____________________________________________________________________________

As always, the opinions shared in this article and the list of gold companies shared that I hold in my portfolio, is definitely not investing advice. I’m not recommending any of these for anyone else to purchase, but rather; I’m simply sharing my opinion on how I view the gold stock sector, and sharing which stocks animate me personally.

Everyone should do their own due diligence, talk to their financial advisors before making any investing decisions, and ultimately make their own decisions on what are appropriate risk speculations and appropriate position sizing. This editorial is simply to illustrate the overriding concepts on why I’ve isolated these types of companies in my own portfolio, and their potential value drivers from my unique vantage point.

In future Substack posts, in the weeks to come, I’ll continue to unpack why I have some of those other aforementioned companies in my personal portfolio. So stay tuned for future updates here, where I continue to dive under the hood on some of these other growth-oriented gold producers, and my take on what separates them from the rest of the pack.

I’ll also have an update out this Sunday with my recurring “Week In Review” summary of key events from this last week. May everyone have a great end to 2023 and another fantastic long weekend with families and friends. Wishing for you all good trading and for life be very prosperous.

Also if you haven’t come over to check out all the interviews we post over at the KE Report, then please come visit us throughout the week and weekend at:

https://www.kereport.com/

Thanks for reading and Ever Upward!

Shad