Opportunities With Mid-Tier And Junior Royalty Companies – Part 8

Opportunities With Mid-Tier And Junior Royalty Companies – Part 8

Excelsior Prosperity w/ Shad Marquitz – 09-21-2024

Welcome back to another update reviewing the opportunities in the mid-tier and junior royalty companies. In the first 7 articles in this series, we established the key value drivers, diversification advantages, risk mitigation advantages, and opportunities for accretive growth over time found in the royalty and streaming companies.

Thus far we have highlighted 8 mid-tier and junior royalty and streaming companies:

Sandstorm Gold (SSL.TO) (SAND), Metalla Royalty & Streaming (TSX.V:MTA – NYSE:MTA), Elemental Altus Royalties (TSXV: ELE) (OTCQX: ELEMF), Vox Royalty Corp (TSX:VOXR) (NASDAQ:VOXR), Trident Royalties (AIM:TRR – OTC:TDTRF), Triple Flag Precious Metals (TSX: TFPM) (NYSE: TFPM), EMX Royalty Corp (TSX.V: EMX) (NSYE: EMX), and Ecora Resources (TSX: ECOR) (LSE:ECOR) (OTCQX:ECRAF).

Here is a link to [Part 7], which has embedded links to the prior 6 articles before that, for the new readers to this channel that may have missed those articles:

https://excelsiorprosperity.substack.com/p/opportunities-with-mid-tier-and-junior-696

In [Part 8] of this series, we’re going to review a few different exclusive interviews and news updates on portfolio companies, as well as introduce a 9th royalty and streaming company on the watchlist.

So, let’s get into it…

Since our last update on royalties, I’ve pointed out in a number of articles when referencing gold that we’ve been seeing major margin expansion in the producers, but also even more impressive margin expansion in the royalty and streaming companies. In the most recent article on gold I mentioned in passing that Sandstorm gold has over $2,000 margins at this point, which is them literally printing money. This will help them accelerate their debt repayment, which has been an overhang on the stock since making 2 key acquisitions in 2022. It was actually a great use of debt, as those acquisitions of Nomad Royalty and BaseCore Metals were well worth the candle, but clearing out that debt using those fat margins is the main focus of Sandstorm for the next couple of quarters.

Sandstorm Gold Royalties Announces 2024 Second Quarter Results - August 1, 2024

Cash operating margins of $2,043 per attributable gold equivalent ounce, representing a new record for the Company, compared to $1,744 per ounce in Q2 2023;

https://www.sandstormgold.com/sandstorm-gold-royalties-announces-2024-second-quarter-results/

There was also a nice news release out of Sandstorm earlier this month summarizing the pipeline of development and near-term production assets, laying out the pathway forward for future revenues:

Sandstorm Gold Royalties Provides Updates on Near-Term Development Portfolio - September 5, 2024

With regards to Metalla Royalty & Streaming (TSX.V:MTA & NYSE:MTA), my partner over at the KE Report, Cory Fleck, had a good interview with CEO Brett Heath, discussing their most recent financial results and some of their key royalty partner updates.

Metalla Royalty & Streaming – Q2 Financial, Corporate and Asset Update, A Look Ahead to H2 2024 - August 26, 2024

Elemental Altus – Q2 2024 Financials, Royalty Project Updates At Diba, Karlawinda, Bonikro, Wahgnion, Caserones, and Cactus - August 30, 2024

David Baker, CFO of Elemental Altus Royalties (TSX.V:ELE – OTCQX:ELEMF), joined me on August 30th to review their operational and financial results from Q2 2024, along with some key royalty project updates at Diba, Karlawinda, Bonikro, Wahgnion, Caserones, and Cactus. We also discuss where the growth will be coming from, within their existing royalties portfolio, as well as the types of future acquisitions the team is working on.

Vox Royalty – Reviewing Q2 Financials, Royalty Partner Project Updates, And The Rerating Potential

Kyle Floyd, CEO and Chairman of Vox Royalty (TSX: VOXR) (NASDAQ: VOXR), joined me on August 15th, to review the key metrics and takeaways from their Q2 2024 financials, a few significant royalty partner project updates, and the potential for a valuation rerating that is more in line with peers and based on their growing revenues.

EMX Royalty Announces Q2 2024 Results; Adjusted Royalty Revenue up 49% YoY - August 12, 2024

Adjusted revenue and other income increased by 32% compared to Q2 2023

Adjusted royalty revenue increased by 49% compared to Q2 2023

Fifth consecutive quarter with positive adjusted cash flows from operating activities

Timok generated royalty revenue of $1,586,000 in Q2 2024 for a second consecutive quarter of record production from the upper zone

Lundin Mining increased its ownership percentage in Caserones to 70%

I provided more details, since I wasn’t able to get something recorded with CEO Dave Cole last month on their Q2 financials, but did just have a nice lunch with both Dave and General Manager of Exploration, Eric Jensen, in Beaver Creek, CO last week at the Precious Metals Summit. Eric shared some encouraging work the company was doing with regards to continuing to build out their portfolio of properties for option, and he put a little more color around the exploration programs that had been announced by their royalty partner operators at their producing assets.

For those that missed the prior interview with Dave Cole from a couple months back, it was more big picture in nature and still very germane for distinguishing the EMX Royalty value proposition. The discussion included a number of copper, gold, and critical minerals partner project updates, a review of other revenue-generating pre-production royalties, Q1 financials, and the balance between further paying down debt in tandem with buying back Company shares.

EMX Royalty Corp – Multiplicative Optionality Across 170 Precious Metals And Critical Minerals Royalties – 06-27-2024

The other royalty and streaming companies reviewed in prior articles like Trident Royalties, Triple Flag Precious Metals, and Ecora Resources were watchlist companies, and so won’t get included in these pieces every time, but I’ll provide updates on them periodically.

To that point here’s an important update: Trident Royalties was officially acquired on Sept 2nd. The initial news of the transaction being announced broke not too long after featuring it here back in [Part 5] in early June of this year. As a result, we aren’t going to be doing any further updates on that company moving forward, but may keep up with Deterra. This also points to the continued consolidation and ongoing M&A we’ve seen in this tiny sector of the resource world.

Recommended Cash Acquisition Of Trident Royalties PLC by Deterra Global Holdings Pty Ltd

https://polaris.brighterir.com/public/trident/news/rns/story/wkdg2yr

Now it is time to introduce the 9th royalty and streaming company in this series, Empress Royalty (TSX.V:EMPR – OTCQX:EMPYF).

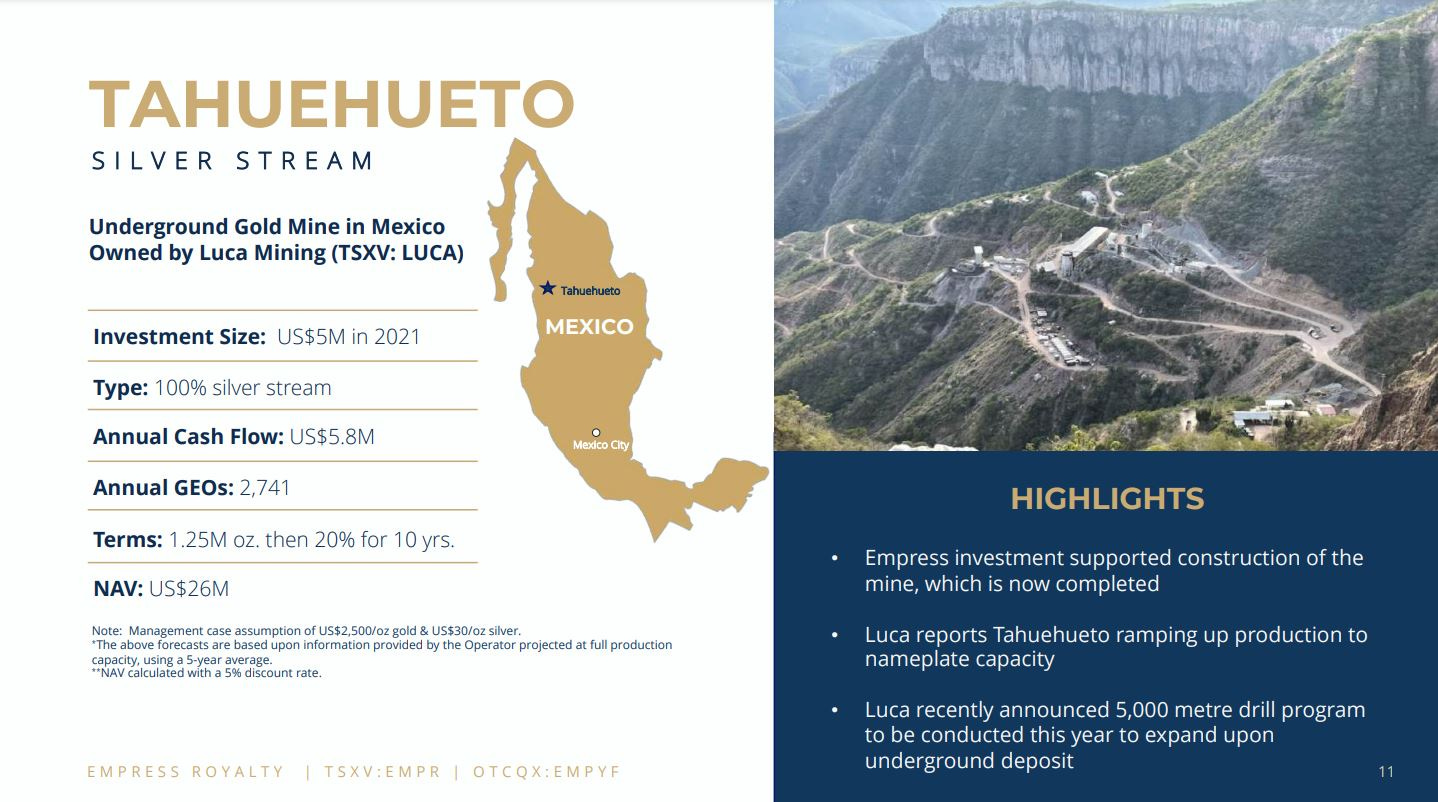

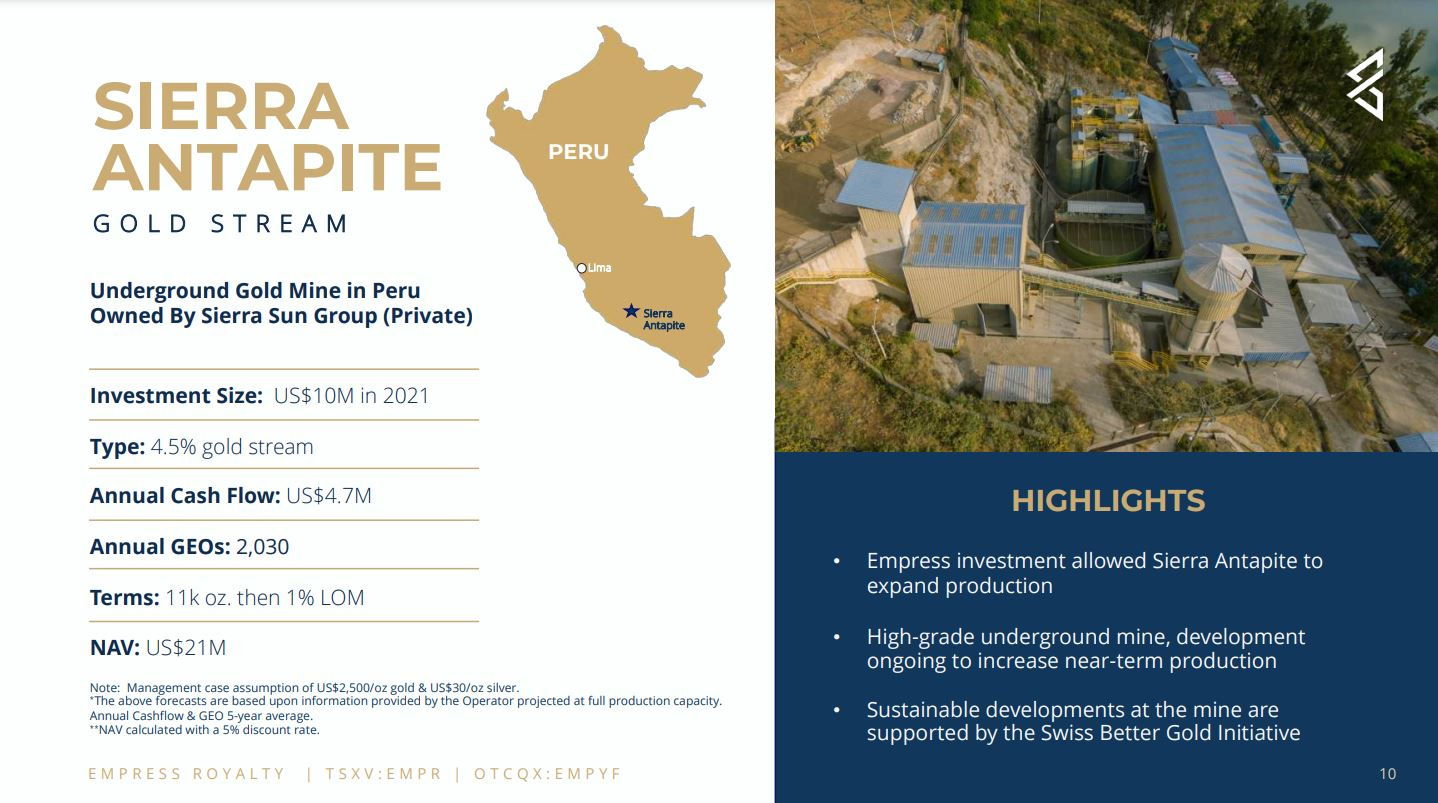

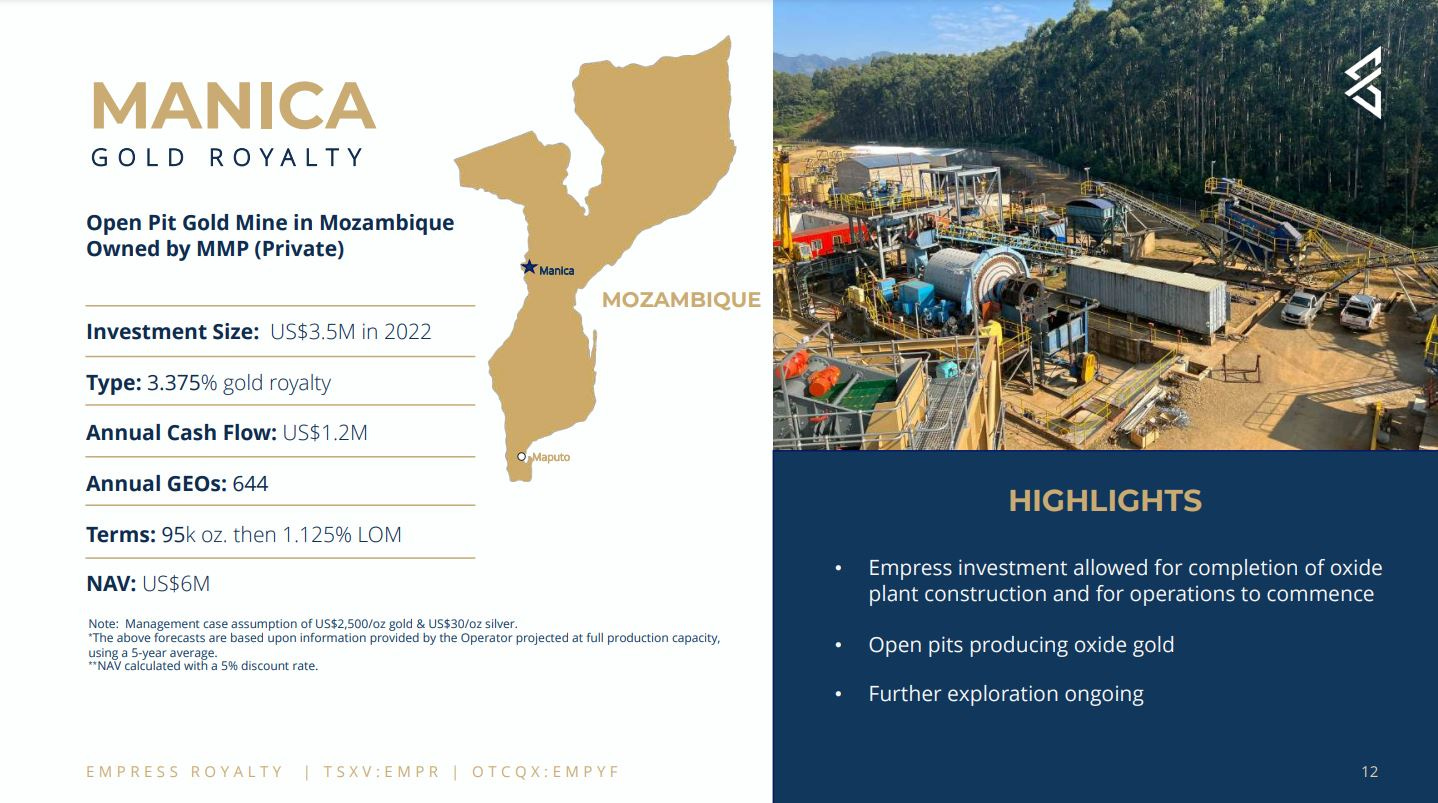

I’ve been following the progress of Empress Royalty for the last couple of years and first spoke to management back in 2022, when they only had 2 producing assets. Over at the KE Report, we introduced them to our audience back in February of 2023, when they then had 3 producing royalty and streaming assets. Today the company has 4 producing assets, with 2 gold streams, 1 gold royalty, and 1 silver stream. They also have one more development stage gold silver royalty, and then a basket of royalties on earlier-stage exploration projects, that don’t receive any significant value presently.

We just had the CEO, Alex Woodyer Sherron, back onto our KE Report podcast on August 23, 2024, to provide an update on the Company’s revenue expansion with these 4 producing royalties and streams. In addition to a brief review and update on each of those assets, we also had her outline the company growth forecasts, both organically and through the future creation of royalties and streams.

Alex also talks about restructuring the debt facility with Nebari Natural Resources Credit Fund I LP and the anticipated revenue growth, forecasting around $6 million by the end of 2024. The discussion covers Empress Royalty’s global approach to project financing, particularly in often-overlooked jurisdictions and the strategy to operate with smaller investment sizes to assist companies from development to production.

This interview is a great jumping off point for readers new to the Empress Royalty story.

Empress Royalty – 4 Producing Assets, Looking To Grow The Asset Pipeline Through Creation Of Royalties and Streams

With that company overview and update as a primer, let’s now dive into the key company fundamentals and their royalty and streaming assets in a bit more detail:

First of all, the business strategy of Empress Royalty within the royalty and streaming universe is through using capital to create new royalties and streams. They provide upfront capital to development-stage or producing operators to advance their projects, in exchange for the ability to buy a percentage or stated amount of the precious metals produced at a specific price via a stream, or they get a net smelter royalty percentage on the metals produced within their royalty area of the project.

In contrast, they are not really using the royalty generation prospect generator model (like EMX Royalty, the Altus assets of Elemental Altus, Orogen Royalties, or Altius Minerals), and they are not typically utilizing the royalty purchase model (like Metalla, Vox Royalty, Gold Royalty, or Elemental Altus today). Through royalty creation, they are following a model that has been utilized by some of the larger companies in the space, like Franco-Nevada, Wheaton Precious Metals, Osisko Gold Royalties, Triple-Flag, and Sandstorm Gold. We don’t see that as often within the junior royalty companies. The caveat being that some companies referenced use multiple modalities for sourcing royalty assets.

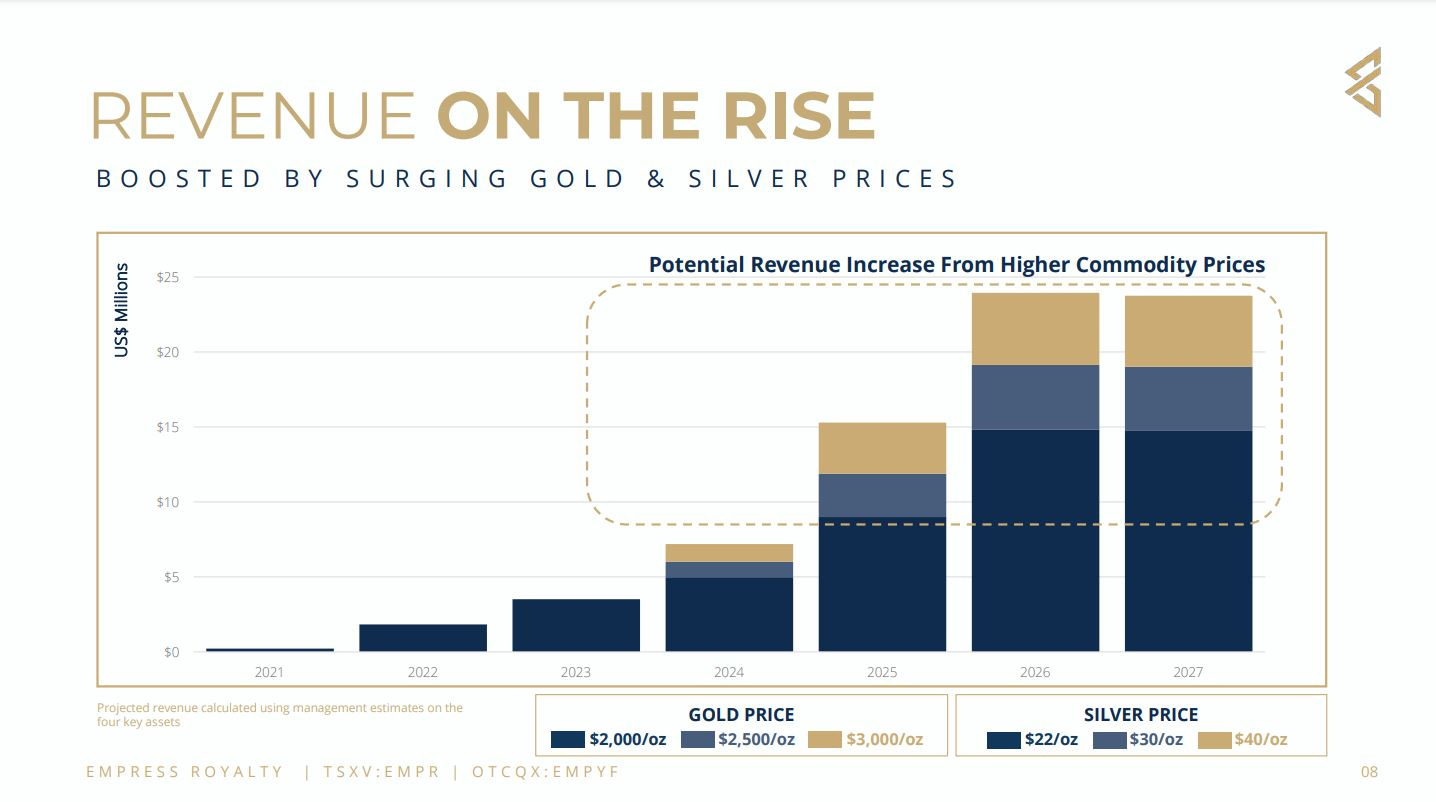

The team at Empress Royalty has done a good job of setting the stage for revenues to rise even in a sideways to down metals price environment, which is one of the benefits of the royalty and streaming business model. However, what impresses me is the sensitivity table showing the revenues at around current levels, using $2,500 gold and $30 silver price assumptions (seen in lighter blue in the graphic below).

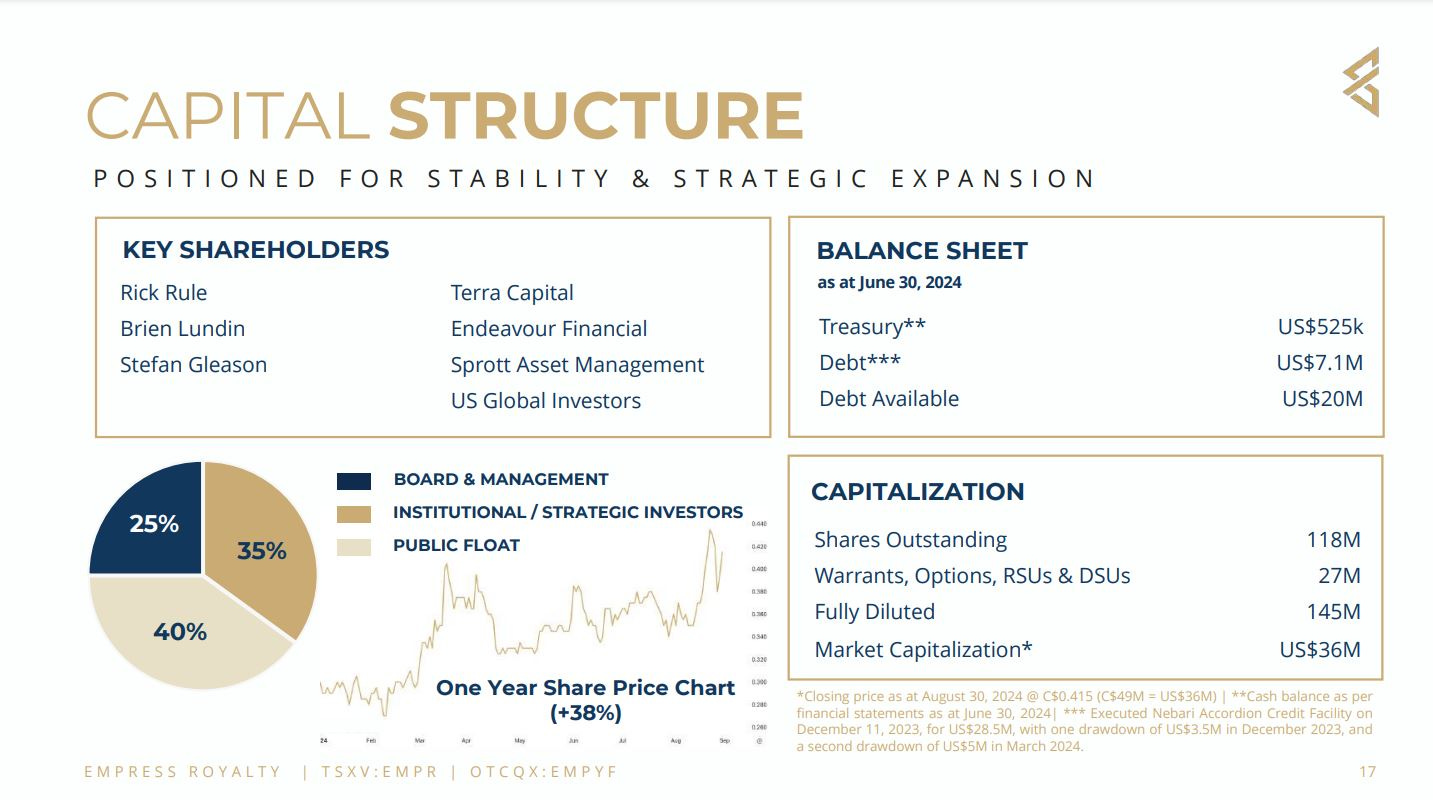

As for the Capital Structure, they are carrying a low amount in the treasury ($525,000 as of June 30th), but do have growing incoming revenues slated to pick up for the balance of this year and heading into next year. Their debt comes in at around $7 million, and they do have a $20M debt facility available to pounce on other transactions. There are 118 million shares outstanding, but 27million warrants, so fully diluted 145 million shares.

I’m also impressed by many of the key shareholders like Endeavour Financial, Terra Capital, US Global Investors, Sprott Asset Management, Rick Rule, Brien Lundin, and Stefan Gleason. Those folks did a lot of due diligence before getting positioned, and in a way have already vetted the company. As a result, I feel comfortable with picking up some shares of Empress Royalty in the future, after I pull profits on some other individual mining stock positions down the road.

Thanks for reading and may you have prosperity in your trading and in life!

Shad