The Precious Metals Sector Is Getting Its Moment In The Sun

Excelsior Prosperity w/ Shad Marquitz (03-15-2025)

It was another noteworthy week in gold, silver, and the precious metals stocks. There are a few interesting things happening with regards to price action on the charts. We’re going to get into that technical action, review a couple specific stock trades from portfolio companies we follow at this channel, and also get some unique commentary from some of the standout PM interviews over this past week. Overall, the precious metals sector is getting its moment in the sun, and it is time to make hay while the sun is shining.

So, let’s get into it…

Let’s kick thing off, as we normally do, with a daily chart of gold:

Once again, we have another all-time daily and weekly closing high locked in on the charts from Friday’s close at $3,001.10.

We also had a new all-time intraday high tagged on Friday up at $3,017.10.

Gold remains well above its 50-day Exponential Moving Average (EMA), which is currently at $2,857.02 and it is still sloping upwards, so that’s still bullish.

What else is there to say until something changes. This chart has been textbook bullish for the last 2+ years.

It may be that gold will need to rest for a bit after probing the psychological $3,000 level to close last week, which would be totally normal approaching a big round number like that. We saw it at both $1,000 and $2,000 on the first attempts. Any pullbacks down near the 50-day EMA would be standard technical action.

Then again, with the backdrop of wild macroeconomic and geopolitical turbulence we’ve been seeing, paired with general equities weakness, then gold could just keep stair-stepping higher until we see more certainty in the markets.

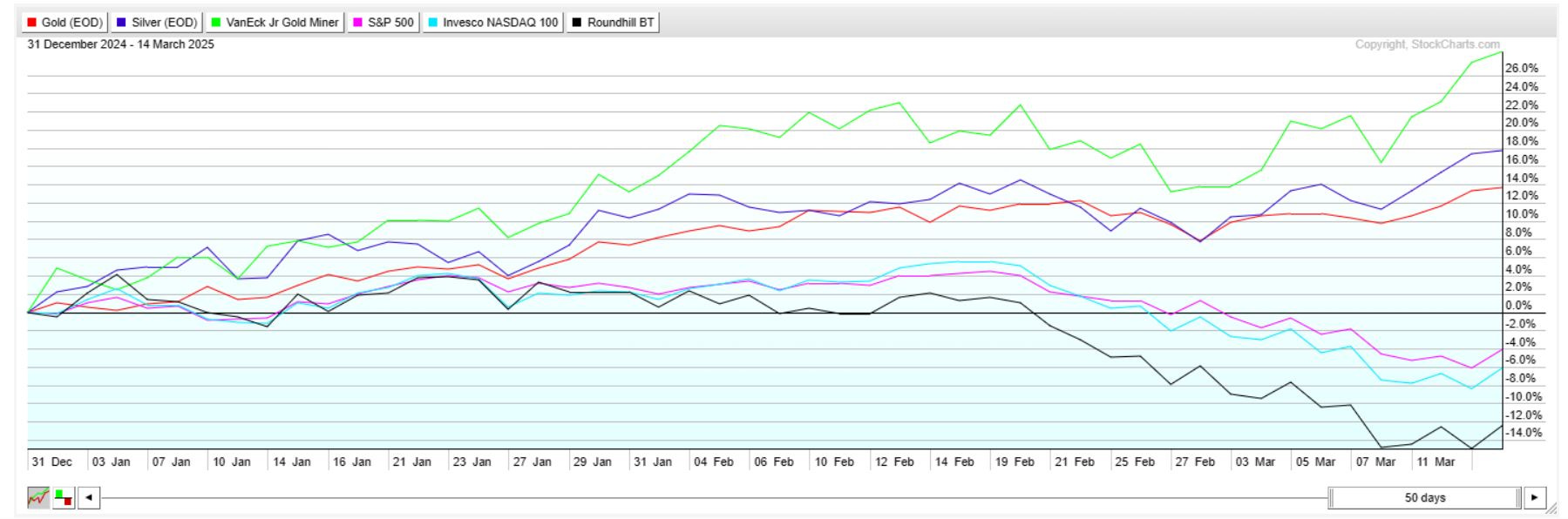

This divergence in the precious metals sector from general US equities in 2025 thus far, and particularly over the last few weeks is worth highlighting. Check out the chart below that features year-to-date price performance action in gold, silver, the GDXJ (for the gold mining stocks), SQM (for the S&P 500), QQQM (for the Nasdaq 100), and MAGS (the Roundhill ETF for the Magnificent 7 mega-cap tech stocks).

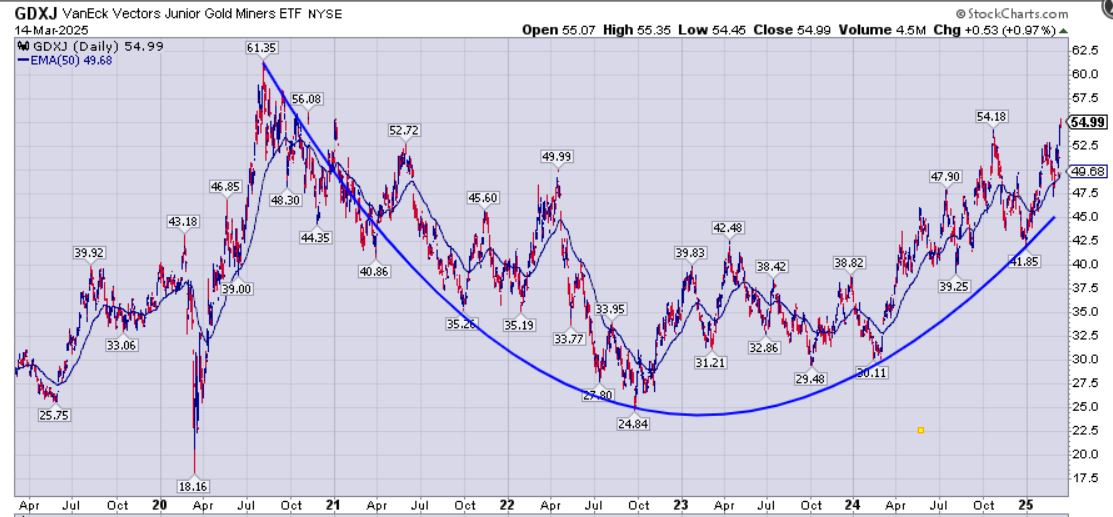

GDXJ has been leading the charge on that year-to-date performance chart, so let’s take a closer look at the technicals on its daily chart:

Friday’s close in GDXJ to the end the week at $54.99, was a higher daily and weekly close than the prior peak at $54.18 hit last October. Also, another intraday high was tagged at $55.35. That is encouraging to see, but not unexpected since gold is at a higher level than that period last year, and the Q4 earnings reports released from many companies were solid; with expectations for Q1 earnings to be even better. A higher-high is undeniably bullish, but we’ll want to see some follow-through.

GDXJ continues to respect the main moving averages for support. The 50-day, 144-day, and 200-day EMAs have offered support more often than not, and so first support on any pullbacks will be the 50-day EMA. At this point, GDXJ is well above that level, so a little cooling off would be normal and healthy. Again, it will depend on gold and, more importantly silver, because if the metals keep ripping, then so will the gold equities.

It is also nice to see the outperformance of GDXJ over gold so far in 2025, and that the gold mining stocks are leveraging the moves in the underlying metals.

If we back up the GDXJ chart we can see that there is a larger rounded saucer-shaped pattern playing out, starting up at the August 2020 peak at $61.25, then dipping all the way down to the late September 2022 bottom at $24.84, and now gradually ascending up that other side, but at a more gradual elliptical rate.

This bodes well that the gold mining stocks can keep ascending back up to that level right above $60 again over the fullness of time, but GDXJ will likely pause and pull back upon approaching the $61 again. Then after that corrective move, it will likely go back up and retest that level again a 2nd or 3rd time until it breaks on through to the other side. I’d anticipate that playing out in late 2025 into 2026, but likely the big breakout would be next year up into more rarified air.

Let’s have a look at the daily-chart for silver next:

Silver’s chart is a bit messier and has more whip-saw pricing action. Friday’s close at $34.43 was marginally higher than the most recent February peak of $34.24, so that is bullish action.

Intraday silver got up to $34.51, which is the highest level this year, but thus far it has not been able to get back above $35. All eyes are on that October peak of $35.07, because that is the next overhead resistance level that bulls will want to see cleared on a daily closing basis (but, preferably on a weekly basis).

Silver is still well above its 50-day EMA (currently at $32.35), so that keeps it in a bullish posture. However, when it gets too stretched above that moving average, then pricing will correct back down to periodically retest that rising EMA.

Now let’s have a look at the performance of silver stocks by way of the (SILJ) daily chart:

SILJ put in a slightly higher close on Friday at $12.28, eclipsing the recent February peak at $12.20, which is mildly bullish. However, the current pricing level in this Junior Silver Miners ETF is still well below the October peak at $14.16. Maybe there is more catchup in store for silver stocks, as the silver price is only just below those same October high levels.

This recent move higher in SILJ has put it solidly above all the key EMAs, and so in a more bullish posture.

Having noted those positive developments, it is a little disappointing how sluggish the silver stocks have been thus far in this leg of the PM bull, but sometimes they’ll just kick it in and make up a lot of ground suddenly. (fingers crossed that we see that play out again).

That red hammer on Fridays trading action is not very encouraging, and often signals a price reversal. Of course, the trend will be primarily affected by the silver price; so if it can solidly break above $35, then SILJ may be able to get some more traction and quickly add on a couple of bucks.

John Rubino, [Substack https://rubino.substack.com/ ], joined us March 13th over at the KE Report, reflecting on the reasons why gold, silver, and the precious metals stocks have continued to outshine the macroeconomic turbulence and general market volatility.

John Rubino – Gold, Silver, And PM Stocks Shining Bright Amidst The Market and Macroeconomic Volatility

We start off discussing the strength in the overall precious metals complex, where silver and the PM stocks have followed gold higher in more an overall flight to safety. John points out that many companies have had positive Q4 earnings reports and wide margins and that data is becoming more obvious to generalist investors that scan for outperforming market segments.

The conversation then shifts to which ways these gold stocks and silver stocks should attract more investors, by either returning capital to shareholders by way of dividends or share buys back, or if they should focus on growth through acquisitions and merger transactions. John wants to see smart transactions, and not just growth for growth’s sake, but feels the building cash reserves of the mining stocks will become large enough that they feel compelled to go out and purchase more mines and more ounces.

Jordan Roy-Byrne, CMT, MFTA, Editor of The Daily Gold, joined me March 12th over at the KE Report to discuss the ongoing divergence between the rally in precious metals versus the corrective move in US general equity markets. This signifies to him that the real precious metals bull market has begun

Jordan Roy-Byrne – The Divergence Between Gold And General Equities Signifies The Real PM Bull Market Has Begun

We reviewed the recent rallies in gold and silver prices, as well as the precious metals equities, in relation to the S&P 500 or the 60 stocks/40 bonds portfolio. We discuss the capital rotation out of growth stocks and into gold and gold stocks, and what a secular precious metals bull market in real terms means for strength and duration of this coming move. Wrapping up we discussed the importance of picking quality PM stocks as the key ingredient for outperformance, versus just being concerned about catching technical turns in the sector.

Dave Erfle, Editor of the Junior Miner Junky, joined us March 11th over at the KE Report to discuss all the volatility in markets as a result of both geopolitical conflict and the economic uncertainty about the global trade wars underway. Gold, silver, and the precious metals stocks continue to be well bid and diverge from the ongoing decline in US stock markets. He believes this illustrates a rotation in capital as investors pull profits out of the highly-valued tech stocks and cryptocurrencies, and then park some of it in the safe haven of precious metals.

Dave Erfle – Geopolitical Conflicts And Trade Wars Are Causing Gold & Silver Stocks To Pop While General Markets Drop

With regards to gold, it is continuing to be well bid above $2,900 but is overbought on the weekly and monthly charts and may be due for a rest. However, it is encouraging to see silver blast back up above the $33 level, and Dave outlined some key overhead resistance levels in GDX and the ratio of gold to US equities that both look ready to break higher in a bullish posture. Additionally, we noted the strength lately in a number of the silver stocks as another indicator that silver and the PM stocks may be signaling an extension of this bullish leg higher.

Wrapping up we discussed some nuances around which type of companies are continuing to get bids from investors. He pointed out that this is not a scenario where the whole sector is rising higher, and it is still important to pick quality stocks with the right fundamental ingredients. Another point raised is how critical it is for resource stocks to get their US listings on a big board exchange, allowing a larger pool of American capital and institutions to drive additional liquidity into their shares. Dave explained that he has a systematic approach and investing rules in place to keep him optimally positioned within his portfolio positions.

Trading Update:

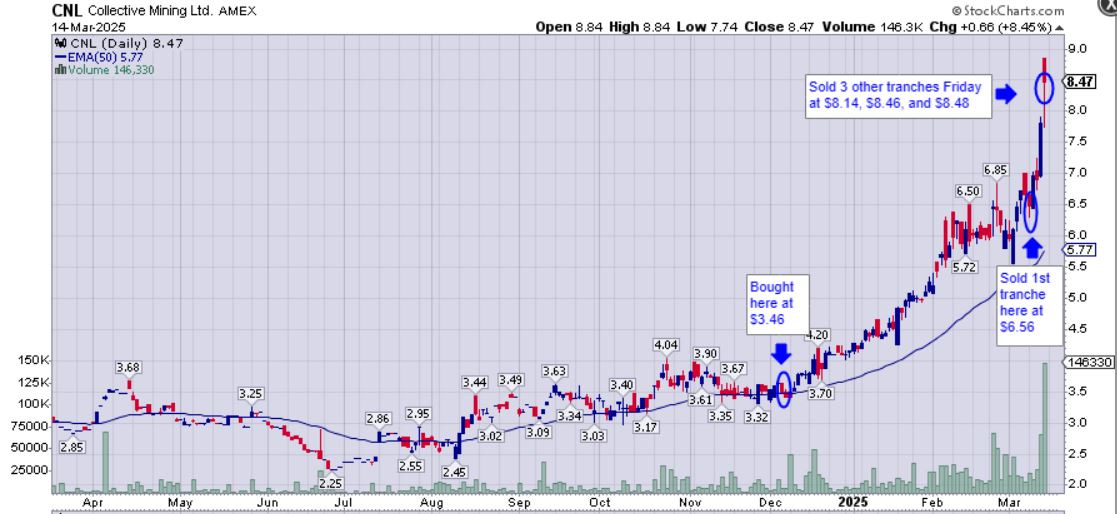

I pulled profits at the end of the week on one of the gold explorers in my portfolio. Collective Mining (CNL) has had a string of really good fundamental news released and consistent best-in-class drill results with high-grade gold intercepts in Colombia. They issued two news releases this last week that were incredibly encouraging and the stock ran bigly on this news:

Collective Mining Drills its Best Hole to Date at the Recently Discovered Ramp Zone by Intersecting 75.80 Metres at 8.01 g/t Gold Equivalent - March 12, 2025

Collective Mining Announces Investment and Early Exercise of Warrants by Agnico Eagle for Gross Proceeds of C$63.4 Million - March 14, 2025

On Friday, I sold out of my (CNL) remaining position in 3 tranches at $8.14, $8.46, and $8.48. Earlier in the month I had trimmed an initial tranche at $6.56, because at that point I’d already had a good run from my $3.46 cost basis that was purchased in December during tax loss selling season. It was beneficial to pull some initial profits, but then leave the core position in place for a move higher. Based on Friday’s wild day – with pricing scorching up higher, then plunging lower, and then rocketing back higher again on heavy volume - I decided to ring the register on this trade… at least for now. The collective win from all tranches combined on Collective Mining averaged out to a 223% gain. Not too shabby on a 3-month position-trade.

Strategy moving forward: I’m always happy to get back into a stock like this with solid fundamental news, if I see a pullback to a level that seems compelling. Additionally, selling into the strength on a chart that has been ripping to the upside is never easy, because the stock can just keep running to much higher levels than anyone envisions. It is quite possible that I left money on the table with CNL, but I felt it was prudent to pull my chips off for now…

My rationale was that the pricing is now stretched well above the 50-day EMA, there was huge volume on a big red reversal candle, and a lot of this bullish news has sucked in more and more buyers of the stock. In this case, I bought the rumor of good drill results to come in December, and I’ve sold the really good news here in March. I don’t know if they can put out a better drill hole than their “best hole to date,” any time soon, but maybe they can… (?)

Now that was really big news on Friday with the best operating gold company on the planet, Agnico Eagle, coming in as a strategic shareholder; and so maybe this thing just blasts into the $9s, $10s, and $11s and I’ll be kicking myself for selling out. That is the risk one takes speculating in the highly volatile junior mining sector.

As an update on 03/18/2025: The CNL stock has gone up almost a buck since I sold it on Friday, just in Monday and Tuesday’s trading action, tagging a high-water mark of $9.39 today. Granted gold has also kept breaking out to even higher and higher levels going up at tagging $3,047 earlier today, so most gold stocks have continued melting upwards. I was anticipating gold to struggle a bit more around the $3,000 level and to see a more of a consolidation week, but we’ve actually seen an acceleration week in the PM sector.

Regardless, I’m not going to cry in my beer if it does keep ripping higher, as I had a really solid trade in this stock. Years of experience has taught me that I’m not going to get hurt taking 223% gains on a stock trade over 3 months. I think Collective Mining does eventually get taken over by Aris Mining, or now maybe even Agnico Eagle, but that could still be a year or two off. If CNL corrects down by 20-30% from here, then I’ll likely re-establish another position. If it just keeps rocketing up to the moon, then my congratulations to shareholders that hang on for the ride!

A second trade on Friday was that I elected to close out of my Equinox Gold (EQX) position at $6.82. It opened strong at $6.94, but stayed under pressure much of the day, and actually sold down to $6.74 in after-hours trading.

Again, just like all sales made into strength, it is possible that I’m leaving money on the table; but between the 2 halves of the position I sold in both February and March my cumulative win on my EQX trade was 212%.

Initially, I had planned to hang onto EQX for the long-game, but as a result of Equinox’s takeover of Calibre Mining, one of my largest weighted gold positions, I’m fine with just holding on to my (CXBMF) and then letting it convert over to EQX shares, when the deal goes through in a couple months.

So in a sense, by way of Calibre, I’m still a shareholder back in Equinox in the near future, and now I’ve freed up cash to reinvest in other companies.

With regards to the Equinox Gold and Calibre Mining merger, I’ve already written about it recently on this channel here:

Merger and Acquisition Opportunities In The Mining Stocks – Part 8

https://excelsiorprosperity.substack.com/p/merger-and-acquisition-opportunities-dbe

On Friday March 14th, over at the KE Report, we also had Ryan King, Senior VP of Corporate Development and IR at Calibre Mining (TSX:CXB – OTCQX:CXBMF), join us to unpack the key takeaways and synergies of the merger with Equinox Gold (TSX: EQX) (NYSE American: EQX).

Calibre Mining – Unpacking The Merger With Equinox Gold To Form A New Major Gold Producer

We started off higher level with how the operating Calibre assets in Nicaragua and Nevada in combination with the Valentine Gold Mine under construction in Newfoundland, will combine with the Equinox Gold assets in Canada, the US, Mexico, and Brazil, and in particular the newly built Greenstone Mine, to form a major gold producer. The “new Equinox” will have a production profile of 950,000 ounces in 2025, and a pathway to 1.2 million ounces in 2026 once the Valentine Mine has ramped up into production.

Next, we have Ryan address the speculation from some Calibre shareholders (including me) that there would have been more value creation by staying a standalone company through the production ramp up of Valentine. Ryan conceded that it could be that staying standalone may have provided more short-term torque as they moved into production at Valentine; but points out that they may also have then missed the opportunity to merge with Equinox, (which was their desired partner that they’ve been in discussions with for many months). Both management teams believe that both companies are quite undervalued compared to peer gold producers on a price/NAV basis, and that by combining that they can unlock the rerating higher.

We also pointed to questions and concerns from some investors about the timing of this announcement and concerns on if there have been challenges with the buildout of this new mine that played into the need to merge. Ryan dispelled the notion that there have been any challenges with the build out of Valentine, as the mine build remains on-time and on-budget, and he stated that was not the rationale for the business combination. Instead, they truly believe that the Equinox assets can be optimized with the strengths of both teams working together to provide a bigger upside value for Calibre shareholders that stick with the pro-forma combined company, compared to any near-term gains they would have received by staying standalone.

Wrapping up we reviewed how elements like jurisdictional diversification, a larger production profile, a larger market capitalization, and a dual-listing on both the Canadian and US exchanges will allow larger institutions and more American investors to participate in enhanced liquidity. Ryan points out that while all those elements will play a part, that it is really more about unlocking the value in the current portfolio of projects over the next few quarters and showing the marketplace why they should be valued at a better price/NAV metric, more in line with higher-valued peers that have even smaller production profiles.

Well, I hope you enjoyed this week’s review of the precious metals sector.

Thanks for reading and may you have prosperity in your trading and in life!

· Shad