Should Investors Consider Holding Commodities Producers Within Their Portfolio?

Excelsior Prosperity w/ Shad Marquitz (03/09/2025)

In this Substack channel we not only review the investment case and price action of the commodities themselves, but specifically the value proposition for related resource companies that produce these commodities, and/or explore for and develop future projects of interest.

This article will be a little different than normal. The goal here will be to explain the rationale and rewards behind being a resource investor, and then specifically towards the end to make the case for why holding some commodities producers inside of one’s portfolio can be a compelling way to make outsized returns.

There are a slew of new articles I’ve been working on to share with readers here, which highlight potential opportunities in gold, silver, uranium, copper, oil, and natural gas companies. However, it occurred to me that we now have a large audience of readers here at Excelsior Prosperity at different points of engagement or investing experience:

• There are likely people that still aren’t quite sure why any of the commodities or resource stocks make any sense for their investment capital, but are open to learn.

• There are people who are just now waking up to this alternative sector, adjacent to general equities or bonds or currencies and want to know ways to invest in it.

• Some people are very familiar with stacking physical gold or silver, but may question why they should put a penny into PM producers or developers or explorers or royalty companies.

These are fair points for consideration. I’m working to release a number of company writeups in the near future, with the mission to highlight compelling value cases in the resource stocks. However, it seems appropriate to take a breather and zoom back from the daily financial noise and minutia and analyze why anyone reading here should take this investment track seriously in the first place.

So, let’s get into it…

In life, we tend to assume that people digest the same information in a similar manner to what we do. We also believe as a conversational default that other people will be totally up to speed on the same topics of interest that we have, share comparable opinions, and understand all the related jargon. This is simply not the case though. Whether the conversation is around topics on political, moral, religious, philosophical, sociological, scientific, technical, or almost any area of life, people are coming at things from wildly different vantage points, levels of study, and understanding. Why would that then be any different with regards to investing?

When we leave the world of small-talk and pleasantries, and get into a more in-depth topics for consideration, then the industry jargon and necessary level of study compounds to where it starts to exclude more and more people. We tend to isolate more people the more granular we get in a conversation, because most folks don’t have that specific narrow focus. Sometimes this overly complex language and terminology becomes a barrier of entry into an engaging field, where others actually would have some interest in it, if they felt the topic wasn’t so difficult to grasp.

I live near Seattle, which is one of the tech hubs in the country and the world. Microsoft, Amazon, Google/Alphabet, and hundreds of other technology companies employee big swaths of the population here, and for some people their whole worlds revolve around these industries. I sometimes hear cross-chatter at restaurants, bars, music shows, health clubs, etc… from the proverbial “tech-bros” living in the area. They are always going on and on about writing code in various computer languages, in-depth back-end processes, cybersecurity protocols, and very specific applications they are trying to resolve.

As an outsider listening in, it is like eavesdropping on a foreign language. Some of those conversations are so peppered with an array of industry terms that one can glaze over like a donut just by listening. While those folks in the conversation may get very amped up and even enthusiastic about these detailed topics, the reality is that most casual listeners would have no connection and no interest in those types of conversations. I see investing jargon in very much the same way…

A funny aside: One of those tech-bro conversations that I overheard occurred inside of a sauna (which are typically quieter places of relaxation and clearing the mind). Finally, a lady beaded up with sweat and perhaps a bit dehydrated after too long in the heat snapped at both of them: “Will you three guys shut up! All this technological mumbo jumbo is hurting my mind. Besides how can anyone else even understand a word of what you are saying?”

I chuckled to myself, and thought, she’s not wrong. Often times, when unpacking investing themes we become those guys spewing mumbo jumbo.

Shortly thereafter, I was attending a mining conference, and a group of us were out to eat and talking shop. Everyone was knee-deep into exploration and development topics, slinging around mining industry jargon and I considered how someone listening in would feel if they overheard our table’s conversation.

“Well the problem is that the recoveries with the sulphides are much more complex than the oxides… Wait, are they just going to heap-leach the surface oxides then and do a carbon-in-leach circuit with the sulphides, or maybe a simpler Merrill Crowe process?... I don’t know, we are thinking since there is coarse gold that maybe we can do a gravity separation circuit first before going to the CIL plant and improve the recovery rates of the gold…. When you go into the second phase underground mining are you going to use block cave or long-hole stope mining?.... Well, the Preliminary Economic Assessment will flush that out but first we have to tighten up the drill spacing for the underground resource from inferred to measured & indicated, due to the NI 43-101 requirements.”

How is this any different than the tech-bros jargon?

Is this way of discussing the mining sector any less isolating for someone new listening in? Does all this complexity inspire new participation?

The extractive industry is its own worst enemy with regards to complicating the overall marketing message and getting stuck in the weeds on tiny conversational thorns. We need to simplify the process for new investors.

Let’s face it, even conversations on general investing can be very much the same way for everyday people listening, when the terminology and concepts are made too complex.

This is true for investing overall with the myriad of different terms to decode (CDs, Money Markets, Fixed Annuities, Variable Annuities, the growing Cash Value inside of Whole Life insurance policies, Traditional versus Roth IRAs, 401Ks, 403Bs, Mutual Funds, ETFs, Inverse ETFs, Leveraged ETFs, short-term versus longer-term capital gains taxes, put options, call options, Consumer Staples or Consumer Discretionary, value versus growth, margin accounts versus cash settlement trading accounts, market orders, limit orders, trailing stops, etc… etc…).

Many people feel that they just won’t ever understand it all, so they let someone else handle what happens to their investment capital. To be clear, for many people that aren’t going to spend the time and effort to educate themselves on how investing works, then turning over money management to a 3rd party firm is a really good option.

However, “letting the fox guard the henhouse” comes with allowing those money managers biases and motivations around their own management fees and commission structures to determine their path forward for your economic future. The results you get will be in line with other clients and retirement accounts returns, but the plan will lack the type of customization or range of options, in addition to the potential for outperformance that comes with managing the weighting and exposure to certain sectors individually.

By way of an analogy, this would be quite similar to the pros of and cons of planning the specific details of your own vacation, versus turning it over to travel agency and paying them a management fee to pick out the activities and make all the arrangements on your behalf.

The travel agency will do well in picking out the standard beach or Disney or cruise or tourist trap vacation, and the itinerary will hit the main highlights other travelers enjoyed; along with picking good 5-star hotels and top-rated restaurant reservations. They line it up so you don’t have to.

The benefits are 2-fold: First, you save all the time and mental bandwidth it would take to do all the research on your own and weigh a number of decisions personally. Second, turning the work over to proven professionals provides the ease-of-mind in knowing your family’s results will be on par with a median to good experience that other families have previously enjoyed.

However, planning your own vacation will allow you to potentially have a more unique experience, tailored to the exact type of events you want to do, the specific benefits and nuances of what you look for in a hotel, the types of restaurants you feel would be most delicious, and a much more individual itinerary. Not only will that vacation be more engaging and rewarding (since you did all the picking of items personally), but you can likely do it all for much less than what the travel agency will charge to set everything up.

The pitfalls of planning your own vacation arise if you don’t consider the details (ie… where is that cheaper hotel located, what are the reviews like about the amenities, is that restaurant going to be open late enough to fit in that other excursion first, was there a better time of year to go to maximize the discounted tickets, where there potential red flags that you missed on first pass, etc…)

To summarize this point, deciding to go out investing on your own versus using a firm to manage your money is much like planning your own vacation versus outsourcing it to the highly-recommended travel agency.

· It can definitely be more rewarding, and more tailored for the exact exposure one wants, but it takes a bit more time to do all the research. There is a reward for the time spent doing due diligence, but it is a sacrifice of time and a willingness to learn.

· When it comes to selecting the components to include in a portfolio or a trip, one can make safe bets that the masses agree with and get average results, or one can make unique choices that could be incredibly beneficial or could turn out to be major disasters. If you want different results than what the masses get, then you have to be willing to take a chance on something that is outside of the norm.

· Errors in judgement can be made that discourage people from trying again, but those should be seen as learning lessons for future trades/trips. Over time you will get better at optimizing the due diligence process, asking better questions, and learning to be more efficient and intuitive with many repetitive aspects.

When people do decide to manage their own money (or at least a portion of their own money), then they first have to decide if they are going to be diversified and to what amount across many types of asset classes from general equities, to bonds, to commodities, to currencies, and now even cryptocurrencies. There are no wrong answers here as far as what sectors to get involved with, or how heavily to weight them, because there a plenty of games to play in the financial casino and many ways to win (and lose).

There are almost unlimited amounts of free and paid resources available for people that want to delve into investing in the general stock market, or options, or bonds, or even currencies. That doesn’t mean it is easy, as one still has to navigate all the specific industry jargon and figure out all the nuanced topics and strategies for themselves. If asked for a guiding hand from a peer working in the financial sector, they will have plenty of opinions and advice on how to approach investing in something like the S&P 500 or Nasdaq, or the 10-year treasury bond, or trading currency pairs like the dollar-yen or dollar-euro.

There is much less educational and instructional material available for those interested in investing in the cryptocurrencies or commodities, and both are seen as more rogue asset classes outside of the investing norm. As a result, few money managers have any experience in the commodities sector or cryptoverse, and if they do, it is normally by way of using ETFs to gain exposure to that space. That means that not only will they be of little help to individuals that want to invest in resource stocks or crypto miners, but they may even discourage people from even attempting to do so, because it is outside of their purview and knowledge.

Let’s focus in on the commodities and resource stocks now, as I’m assuming that is the key interest with readers here in this channel.

Often people will ask me what I do professionally, and when it comes back to commodity investing and resource stocks, they either go into a blank stare back (not sure what commodities even are), or they’ll say “That’s interesting - I don’t know anything about that but really need to focus on investing more…” Sometimes they’ll press me further asking, “Is it like what I do investing in my 401K and IRA at work, or it is more like those people I see trying to get rich in cryptocurrencies?”

I’ll explain that investing in the commodities sector is a bit more volatile, and requires medium-term position-trading into the cyclicality of this space; compared to the longer-term dollar-cost-averaging into the mutual funds and bonds that make up your retirement account at work.

Conversely, while the price action in commodities and related resource stocks can have outsized moves to the upside and downside compared to conventional equities, the sector is not quite as volatile as the very speculative cryptocurrencies. This is because the commodity products are the epitome of hard assets, and not just the greater fool trading of digital ghosts.

In a way, resource investing is a nice counterbalance between the slow and steady general equity markets versus the hip and hyper-volatile digital assets.

They’ll usually give themselves the out for not doing any more real work and research into the topic: “Well, I really wish I knew how to do that, but don’t really know anything about commodities and would just need you to tell me what to buy.” [Then they’ll inevitably ask me for a hot stock tip on where they should put their money.] (palm-to-face)

Most people actually do know precisely what commodities are, once someone simply unpacks it for them. They are crucial to almost every component of life, and one could say they are the “stuff” or “ingredients” in almost everything. Throughout history, the commodities have been a cyclical sector, rising and falling with the supply/demand fundamentals for the particular raw materials that make the world go round. These resources are then funneled into everything we see around us from buildings and homes, planes/trains/automobiles, snowplows/lawnmowers, home appliances, industrial machines, clothing, food, books, toiletries, medicine, toys, defense, and even the electronic devices like the smartphone or laptop you are using to read this article.

There is the old adage: “If it is not grown, then it is mined.”

The reality is that most people are divorced from the process of how products are manufactured or grown to stock the stores near their homes or magically arrive on their doorstop from Amazon orders. The average person will occasionally reflect on the prices of cocoa, coffee, soybeans, cattle, or wheat in the “soft commodities,” grumbling about prices going up at the grocery store. Most folks have a better grasp on farming for foods, or logging for lumber, than they do the extractive industries for oil, natural gas, metals, or critical minerals.

The truth is that nothing someone owns would be here without commodities (yes, even if they are anti-mining). Without mining the necessary metals or energy commodities, then there would be no travel in cars, buses, trains, airplanes, or even bicycles and ebikes. There would be no ovens to cook food on, and no dishwashers or washing machines for clothes; not to mention there would be no electricity to power any appliances. There would not be solar panels, windmills, or lithium batteries either. There would be no manufacturing anywhere without commodities, and there would be nothing for sale in stores or on Amazon (nor would there be delivery trucks to drive these products to your home). Oh yeah, there wouldn’t be modern homes either, and no wiring or plumbing in the homes. Once you break it down for people that way, usually the lightbulb goes off. Commodities aren’t optional, they are necessary.

Once you have the understanding that commodities are volatile but will remain forever necessary, then it becomes a matter of analyzing where we are in a specific commodity’s cycle, looking for good points for entries and exits.

This is best achieved by looking at pricing charts, while still keeping a rough eye on the macroeconomic and fundamental developments within certain sectors.

It is good to be diversified across a mix of commodities, because they are all moving independently and will have different moments in the sun. At any given time a couple of commodities will offer alpha to the rest of the commodities sector beta in relation to the general markets.

Commodities (as an overall group) have been underperforming the general equities (as an overall group) for a long time, but there have still been brief periods of time (several months to a year) where oil, or nat gas, or fertilizers or cocoa, or coffee, or copper, or palladium, or more recently gold, has outperformed general stock market indexes. In this sector, knowing when those individual commodity runs are setting up or underway are crucial to capturing that alpha and outperformance.

The big moves higher in a commodity will not persist and will be fleeting, as the cure for high prices is high prices. Bottlenecks get unwound, substitutions and workarounds are found, and new supply is incentivized to come online. Because of that, I’ve always considered it like a big game of Whack-A-Mole, where one metal or liquid pops its head up, then goes back down, and the 2 or 3 more pop their heads up for a bit and then they go back down, and so on… A resource investor needs to strike while the specific commodity is popping up, because it won’t last forever. There can be outsized gains captured in well-executed position trades over several months to a year.

Once an investor picks out the commodities that they want to study, and begins looking to identify acceleration periods, then those can be traded with futures contracts, or many have specific sector ETFs. For most investors that don’t want to mess with the futures market, then the ETFs or ETNs are the simpler way to invest in a specific commodity’s trend inside of most trading platforms.

These ETFs/ETNs generally track the price action in many commodities:

Oil (USO), nat gas (UNG), gold (GLD), Silver (SLV) (PSLV), platinum (PPLT) uranium (U-UN.TO)(SRUUF), sugar (CANE), coffee (CAFE) (JO), etc…

Let’s get into some more ETF examples here for investors that have decided that they would like to get exposure to the related resource stocks in some of the more popular commodity sectors:

If someone is bullish on oil & gas and the related energy companies, then they can hold the larger producers in the Energy Select Sector SPDR Fund (XLE), smaller producers, developers, and advanced explorers in the SPDR S&P Oil & Gas Exploration & Production (XOP), or various oil service companies like drillers, pipeline, refiners, and energy-tech companies via the VanEck Oil Services ETF (OIH). Those 3 ETFs move and can be traded independently, but pretty much give an investor exposure to the whole traditional energy sector.

If someone is bullish on copper stocks then there are a few good ETF options: Global X Copper Miners ETF (COPX), iShares Copper and Metals Mining ETF (ICOP), Global X Copper Producers Index ETF (COPP), Sprott Junior Copper Miners ETF (COPJ).

For exposure to uranium producers there are 3 good ETFs the Sprott Uranium Miners ETF (NYSE: URNM), the Sprott Junior Uranium Miners ETF (Nasdaq: URNJ), and the Global X Uranium ETF (NYSE: URA).

If someone is bullish on the silver producers then there are there are 2 widely followed ETFS: Global X Silver Miners ETF (SIL), and ETFMG Prime Junior Silver Miners ETF (SILJ), and a 3rd one gaining some more traction lately the iShares MSCI Global Silver Miners ETF (SLVP). It should be noted that that unlike the oil, copper, and uranium producers the silver producers are not as contained to just silver, because there are a number of gold and base metals focused companies also mixed in the companies selected. Silver stocks are tough, because most deposits are polymetallic in nature, but these ETF vehicles will generally still leverage the price action in silver.

Then with Gold there are a number of ETFs that contain gold producers: VanEck Gold Miners ETF (GDX), VanEck Junior Gold Miners ETF (GDXJ), Sprott Gold Miners ETF (SGDM), Sprott Junior Gold Miners ETF (SGDJ), and Global X Gold Explorers ETF (GOEX). Don’t let the names like “junior” or “explorers” throw you off with these thought. All of these ETF are mostly filled with the larger and mid-tier precious producers.

For brave investors that are comfortable taking on more risk, but also potentially have outperformance beyond the ETFs, then they can get positioned directly in the actual producing companies themselves. This provides leverage to the underlying commodities in both directions.

If people want some initial ideas, then a simple process is to deconstruct the company holdings inside of the ETFs mentioned above. It is easy to see which companies the fund managers have placed the heaviest weightings on. However, experience has taught me, that doesn’t mean those will be the best performers over a given time period. In many past cycles it has been the smaller weighted companies, (or even companies that are not even featured in the ETFs), that have more associated risks, but that ended up being the outperformers.

This is where the individual portfolio construction is crucial as one builds their own ETF of solid mining stocks. This involves more research and due diligence than just buying an ETF, to ascertain each individual company’s particular edge versus a basket of their peers. Here are some good questions to consider:

What were the recent revenues and free cash flows? Also look at metrics like free cash flow per share, EBITA, price/enterprise value, price/book value, and price/NAV. There can be noticeable disconnects in the small/medium producers.

What are their cash costs and all-in sustaining costs (AISC)? What is the trend in these costs over the last few quarters or years? Importantly, what costs are being guided for the quarter and year ahead by the company? See the future now…

What are the overall mineral resources and reserves for the company? (Reserves have higher confidence in being mined and resources may fall into several categories of various degrees of confidence). With oil companies it will be proven and probable barrels of energy equivalent.

What is the remaining life at each mine, based on their technical reports? For oil/gas companies it will be more around understanding what their well decline rate is (this reflects how quickly they are being depleted and future well life).

What is the jurisdiction and is there an appropriate premium or discount for operating in that area of the world, country, or state/province factored in?

What is the upside case for development projects or exploration projects? Essentially, what is the growth case for the company organically, within their own projects, and are some of these not being valued appropriately?

Maintaining a heavy weighting inside my resource portfolio in the mid-tier and small producers has always been part of my personal approach in this sector; ever since transitioning from investing in general US equities over to the wild and wacky world of speculating on resource stocks back in 2010. It didn’t matter whether it was gold, silver, copper, oil, natural gas, lithium, or uranium – I wanted to be positioned first and foremost in the actual producers of those commodities.

Of course, there are still fantastic opportunities in the developers, advanced explorers, and early-stage greenfields explorers. We do have a number of different series on this channel that also delve into those stages of companies, and my preference is to be diversified across various stages of resources stocks to capture different risk/reward opportunities at different points in the cycle.

I want to wrap up here with some observations about how the precious metals investors often approach investing in the gold and silver equities much differently than other commodity sectors.

Oil bulls buy oil producers first. Natural gas bulls buy nat gas producers first. Base metals bulls in copper, nickel, iron, zinc, etc… buy the larger base metals producers first. Uranium bulls typically are invested in the limited number of producers first. These investors may still speculate on the earlier-stage companies exposed to exploration and development, but those are positioned in smaller sizes, as the riskier investments that they are. Precious metals investors, often times will implement the reverse of this philosophy, and to mixed results…

It has always been curious to me that so many precious metals sector pundits, newsletter writers, and fellow resource investors, that I’ve met over the last 15 years, have very small allocations to the gold and silver producers or some ironically have no exposure at all! With gold and silver there are just so many pre-revenue junior companies (over 1,000) that are all out marketing and filling up the show floors of convention centers. The problem is that many of them don’t have much gold or silver.

Because there are so many more pundits in this space trying to distinguish themselves, they try to pick those tiny junior companies that are very high-risk / high-return potentials, with the hopes that it becomes a multi-fold gainer in the right environment, or maybe even one of those legendary “10-baggers.” This gets the largest number of investors chasing the riskiest end of the sector and for decades has created a small minority of big winners, but sadly many more investors that have swung for the fences on too large of a position size and lost big. Those investors then get impression (and trumpet it loudly to others) that investing in precious metals equities doesn’t work. Sadly, they rarely consider their risk profiles, or position sizing, or even have a deep thought as to what they’ve actually invested in.

As a result, many gold and silver investors neglect getting into producers first, and sometimes find themselves holding baskets of junior stocks that are 100% pre-revenue generating companies, and often without much bankable gold or silver in them. These are the “penny dreadfuls” that other pundits have warned against, but they continue drawing in new hordes of investors each year.

This is quite odd because the primary leverage that resource stocks provide to rising prices in their underlying commodities are from extracting those valuable resources from the ground and then selling them for a profit with expanding margins. One would then surmise that PM investors, who are already typically more risk adverse (which is what had them gravitate to sound money and hard assets in the first place) would be most heavily positioned first into the producers, if they are bullish on gold’s price trajectory.

The reality though is that it is all too common to speak with people that are mostly or totally positioned in only drill plays or maybe some companies advancing deposits towards economic studies. Some will flat-out turn up their noses to holding a company in their portfolio that is actually pulling the commodity (that they claim to be bullish on) out of the Earth and selling it. Strange.

However, it should be pointed out that pre-discovery or earlier-stage exploration companies don’t have initial leverage to rising commodities prices, because they don’t have economic resources in the ground with mines extracting those stated resources with expanding margins.

Instead, those exploration companies will rise and fall due to their newsflow, if they are able to build value or if they end up destroying shareholder value. The commodity price direction only offers a headwind or tailwind to their newsflow.

Most retail investors don’t think this point through all the way, and then at each sector turn higher we always hear them come out and lament that their junior stocks are not moving higher with gold or silver or copper or uranium. Why should they? There aren’t bankable economic ounces or pounds in the ground yet.

Many resource investors have become so completely mesmerized by the thrill of exploration that they really have tunnel vision in that regard. That is fine to have a focused approach. I totally get it if they are geologists and rock nerds that love the thrill of the “treasure hunt.” Treasure hunts are ridiculously fun, but that is not nearly the same thing as producing the treasure and then selling it.

This approach that so many have embarked on over the years is much different than having direct exposure to the commodities or their price direction. Exploration companies only have land, a scientific thesis, hope, and the capital they raised from investors… and they are not yet backstopped by true intrinsic value underground.

I also get it if some people aren’t really interested in investing in a leveraged play on the commodity price action. Some folks also don’t want to mess with learning about all the components and different risk factors and benefits that go into the operation of legitimate revenue-generating mining businesses in the resource sector. Just like any investing sector, it is not for everyone.

Some people are more gamblers than investors, so I understand that they are swinging for the fences on the potential of a tiny team to make new discoveries, and they are using speculative funds that they don’t mind losing… (They typically will lose much of those speculative funds in the event that those companies fail to hit significant paydirt and are left with just subeconomic dirt – so there is no intrinsic long-term value backing drill plays other than the surface value of the land they staked).

There is nothing wrong with taking a punt on a high-risk/high-reward speculation, because the potential payoffs are quite intoxicating. Speculating in a discovery is a binary outcome bet though, with big winners, but mostly sub-par losers. Sure, it can be quite thrilling when exploration yields a true success story. Again, I love the thrill of a true discovery hole as much as the next punter. Exploration just needs to be thought about rationally, within the context of what the odds are of actually making a discovery of a true economic project.

To be crystal clear, I’m not suggesting that those resource speculators that are only invested in explorers are doing it “wrong.” Some folks strictly like the early-stage part of the industry. Many of them would point out that some of the biggest gains in the sector will come from the explorers that make a new discovery. Absolutely, that is 100% true. It is also just as true that 99% of the explorers won’t make significant discoveries that turn into an economic producing mine or wellfield. It’s a gamble, and really Las Vegas has better odds.

If the early-stage explorers don’t find an economic deposit of interest, then they have to go right back to the drawing board and raise more money, dilute the stock, and test the next thesis and target, (or they have to switch properties). In the end, either the exploration company makes a true discovery that can be sold or developed into an economic mine, or they simply have mined the capital markets with dilutive financings to provide themselves highly-paid jobs.

There are some really competent teams in the exploration space, that are doing excellent work, but nobody knows what is underground until the drill bit (truth machine) brings back the assays. Even then, it could just be that they drilled the wrong direction, or not deep enough, or stepped out the wrong direction, or many other factors. Exploration is very tough work, and I respect the teams that can efficiently test their thesis, or that seem to be onto something special.

As long as somebody understands the risky bets they are taking with explorers, then more power to them. However, it would be incorrect to consider them investing in the commodities when most of those companies don’t yet have meaningful economic concentrations of the commodities defined in the ground. Some of the developers with both resources combined with economic studies do have enough data collected to have optionality to rising precious metals prices.

When I hear people taking on debt to go “all-in” on a grassroots exploration story, or if they are funding their lottery ticket positions on credit cards to speculate on coming drill holes, then it does make me concerned that they haven’t fully grasped just how risky those bets actually are.

Some people will work to limit the risks by diversifying across 10-20 exploration companies (knowing most won’t deliver the goods, but hoping 2-3 do so in an outsized manner), and they filter for good management teams, jurisdictions, and attractive types of deposits being tested. This is at least a way of having a systematic approach, and I know investors that have done incredibly well using a process like that. It still boggles my mind when they don’t have any actual producing companies in their portfolios though.

Even at resource conventions, most of the companies featured are explorers or developers, with a far fewer number of producers that exhibit. I believe sometimes this gives retail investors the erroneous idea that you don’t want to be in the producers, and to spread your money around to a few dozen pre-revenue companies and see if any of them “get lucky.”

The broader point being made here is that so many “resource investors” are mostly or completely positioned in companies that are essentially poking holes in the ground to try and find something of value. They are often positioned like this at the exclusion of being positioned in the companies that are actually pulling the commodities (the treasure) out of the ground and producing real revenues. It is just an unusual market sector, as most other sectors are dominated by companies that sell a product or service for profit.

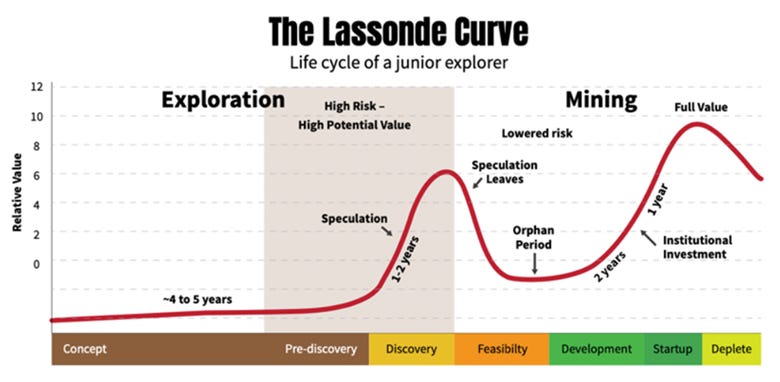

One other point to make, is that we must also dispel a silly notion that pervades the gold mining stock investing sector. This erroneous belief system is due to a misinterpretation of the Lasonde Curve. Retail PM investors like to parrot back to one another that the only 2 places to make big gains are in the discovery stage, or in the pre-production sweet spot. Some maintain the erroneous belief that once a company becomes a “producer” that it is then “fully valued” and at the end of it’s journey as an investable asset, setting up for depletion and closure.

• Please don’t mention that to Hecla Mining that has been in business over 130 years, or Newmont Mining that has been in operations for over 100 years at this point, with both companies growing and continuing to build value through acquisitions during different phases and market conditions along the way.

• This notion that producers are all fully valued and at the end of their journeys is, of course, complete rubbish. There a plenty of times in this more recent bull market, that started when Gold bottomed in December of 2015, where it was actually the small to mid-tier producers that had the biggest percentage gains on sector rallies as a collective group of stocks. In fact, many junior explorers or developers barely budged during those epic moves higher in the sector, whereas most producers shot up high double-digits to solid triple digit gains.

• To suggest a company is fully valued once it does first pour and graduates to a legitimate revenue generating business is utter nonsense. Clearly that revenue-generating company can use those funds to keep developing the optimization processes for the first mine to lower costs and improve margins. They can use these revenues to increase development and run higher throughput of ore into their processing center. Other companies have plowed revenues into seeking out higher grade areas of the deposit to then mine, increasing recoveries, and improving production metrics. Keep in mind that this is all just on the initial mine they have, and doesn’t account for companies that develop or bolt on additional mines for better size, scale, efficiencies, cost of capital, stock liquidity, and so on.

• In addition to optimizing an initial mine, a producing precious metals company may then opt to grow organically by using those mining revenues to bring another mine into production in it’s development pipeline.

• Another option for more value creation is to additionally grow through acquisitions and by picking up other producing or development-stage projects from other distressed companies, or simply non-core projects from larger companies.

• Lastly a company with revenues, can then fund part of or all of it’s exploration through the ATM machine of it’s producing mine or mines. This self-funded exploration can thus expand the company resources, leading to either increasing production output or extending the mine life. Those familiar with the gold production space can think back to how Newmarket Gold/Kirkland Lake (now held by Agnico Eagle) was transformed by a massive discovery at depth at the Fosterville Mine in Australia. Other examples would be the transformative discoveries that Anglogold Ashanti, Wesdome, K92 Mining, Karora Resources, and Calibre Mining made that showed they had far more growth and value creation in front of them, than when they initially made first gold pour.

• All of these different ways to generate more value and “alpha” can lead to a given producer seeing it’s valuations and share price heading much higher for a period of time or even longer stretches of time in a good metals price and sentiment environment. When companies graduate to revenue generating producers, they are far from fully valued, and often have only begun their real growth trajectory.

Thanks for reading and may you have prosperity in your trading and in life!

Shad